Picture this: 22 years. That’s how long BAE Systems (LON: BA) has hiked its dividend without a single miss — including the Covid pandemic, when roughly half of FTSE firms saw their payouts disrupted. Severn Trent (9 years) and Standard Life (LON: PHNX) (10 years) are doing the same thing more quietly. While the FTSE 100’s high-flyers grab headlines, these three pay steady, growing income to investors. Here’s what makes them tick.

BAE Systems: 22 years of hikes through every market

Tier 1 supplier status with the biggest defence spenders — the US and UK — locks in multi-year contract visibility most companies can only dream of.

BAE Systems (LSE:BA.) has hiked its dividend every year for 22 unbroken years. The streak survived the Covid pandemic — when roughly half of Footsie firms saw their payouts disrupted, BAE just kept paying more. On top of that growth, the stock has delivered a 3.7% 10-year average yield to long-term holders.

What’s behind the consistency? Tier 1 supplier status with the biggest defence spenders — the US and UK — locks in multi-year contract visibility most companies can only dream of. Massive barriers to entry (designing and building fighter jets isn’t a Saturday project) keep competition thin and protect long-run pricing power. And a diversified product range across air, sea, land, and cyber softens the impact of any single programme slowdown.

The bigger tailwind is geopolitical. Global defence budgets are climbing, flowing straight through to BAE’s order book. The fighter jet programmes, naval contracts, and missile systems that sit on its books today are multi-decade revenues, often inflation-linked.

That’s the kind of pipeline that funds a 22-year dividend streak — and the order intake suggests it’s not slowing down. The diversification across services and platforms also means the income stream isn’t tied to any single customer or contract cycle.

Severn Trent: the water monopoly that just keeps paying

Severn Trent (LSE:SVT) is the most defensive name in the trio. Water supply is a service nobody can cancel — and Severn Trent’s water reservoir and pipe network covers the Midlands region of the UK as a regulated monopoly. No real competitive threat exists, by design.

Add in multi-year regulatory periods that lock in revenue and capital plans, and dividend visibility becomes hard to match elsewhere on the index. The 9-year unbroken dividend streak and 4.2% 10-year average yield sit on top of one of the most predictable cash-flow profiles in the FTSE 100. The asset base keeps growing every year — and a growing asset base mechanically feeds higher dividends, because regulators allow a return on it.

The catch is debt. Regulated utilities carry heavy capital-spending loads, and rising rates push borrowing costs higher. The company has been through rate cycles before, though, and a strong operational efficiency record limits how much pressure flows through to the bottom line. The dividend hasn’t blinked yet — and the regulatory framework makes a cut harder here than for almost any other listed business.

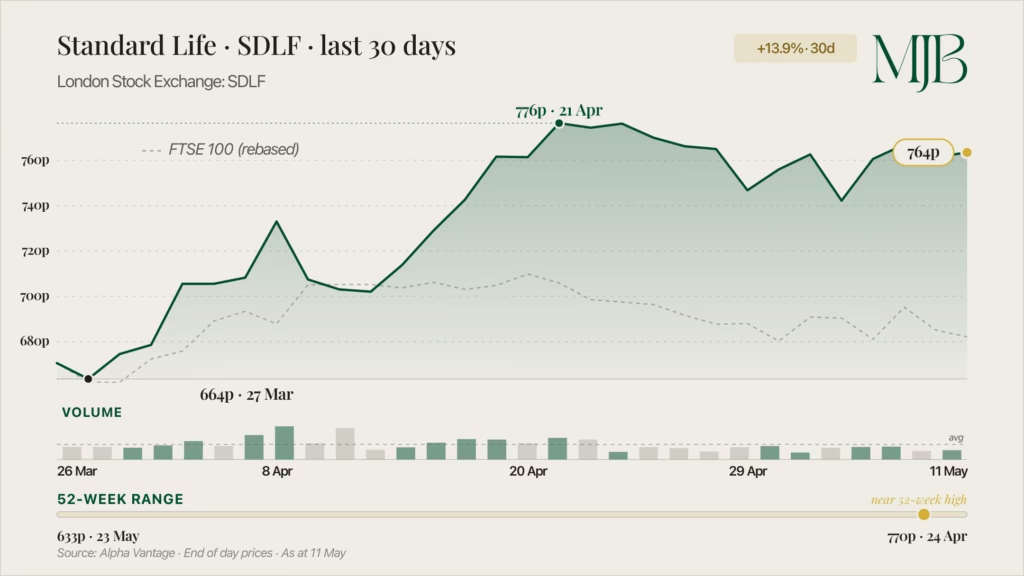

Standard Life: the income outlier

Standard Life (LSE:SDLF) sits at the high-yield end of the trio with a 7.5% 10-year average yield — well clear of the FTSE 100’s 3%-4% range. The reason isn’t financial engineering; it’s the business model.

The company buys “closed” life insurance and pension policies, then runs the existing book down predictably. Cash flows are tightly hedged against interest-rate moves. Capital-light operations mean less reinvestment, more of the cash hitting shareholders’ pockets. Its Solvency II ratio sits at 176% — well above regulatory minimums and a clear signal that payout capacity has room to keep growing.

The dividend record is 10 unbroken years of growth, and the structural drivers haven’t weakened. The UK retirement and savings markets are getting bigger as the population ages. Demand for capital-light annuity providers is rising. The income premium Standard Life delivers isn’t easily replicated by a high-street insurer — which is exactly why the yield gap to the FTSE average persists.

The risks worth watching

No share is risk-free, and these three have specific pressure points. BAE Systems’ earnings could suffer if defence-related supply chain issues worsen, impacting future dividend hikes. Standard Life faces rising competition in pensions and annuities — a structural pricing pressure that’s grown teeth over the past decade. And Severn Trent’s profits could take a hit if interest rates rise and borrowing costs shoot up.

These are headwinds, not breaks. The underlying business models — Tier 1 defence supplier, regulated utility, closed-book insurance — are still some of the most predictable cash generators on the index. On the past decade’s evidence, this trio is far more likely to keep hiking dividends than to cut them — even as new shocks land on the FTSE.

The Bottom Line

Make no mistake: past dividend hikes aren’t a guarantee. BAE faces supply-chain risk, Standard Life rising pensions competition, Severn Trent higher rates. Yet over the coming months, expect this trio to keep paying — and rising. Watch for the next dividend declaration. You might find these are the income names worth holding while the growth side of the LSE-boku-lse-underrated-growth-stocks/) chases the next listing move.

Want more like this? Sign up to The MJBurrows Briefing — our free weekly newsletter delivered every Monday morning.

FAQ

Why does BAE Systems pay such reliable dividends?

BAE’s Tier 1 supplier status with the US and UK defence ministries gives it multi-year contract visibility, and high barriers to entry shield its margins. That combination has funded 22 consecutive years of dividend hikes — and the order book backs further ones.

Is Severn Trent’s dividend safe if interest rates rise?

Regulated water utilities like Severn Trent carry heavy debt loads, and higher rates do raise borrowing costs. But its 9-year unbroken dividend record and multi-year regulatory periods mean payout cuts would be the last lever the board pulls, not the first.

How does Standard Life deliver such a high yield?

Standard Life’s closed-book life and pension model generates predictable cash from in-force policies, with capital-light operations meaning more of the cash flows through to shareholders. A 176% Solvency II ratio also signals room for further payouts, not pressure to trim them.

Disclosure & Editorial Standards

MJBurrows is not authorised or regulated by the Financial Conduct Authority (FCA). The content on this website — including articles, calculators, and tools — is for general informational and educational purposes only. It does not constitute personal financial, investment, tax, or legal advice and does not take into account your individual circumstances, financial situation, or objectives.

Nothing on this site is a personal recommendation to buy, sell, hold, or otherwise deal in any financial product, asset, or service. You should always conduct your own research and seek advice from a qualified, FCA-regulated financial adviser before making any financial decisions.

Our calculators produce estimates based on simplified models using HMRC-published rates for the current tax year. They cannot account for every individual circumstance and should not be relied upon as exact figures. Tax rules and rates may change — verify current rates with HMRC or a qualified tax adviser.

Projections are not guarantees. Where our tools show future values (investment growth, pension projections, compound interest), these are hypothetical illustrations based on assumed growth rates. Past performance does not guarantee future results. The value of investments can go down as well as up.

Market data displayed on this site is provided by third-party sources including Twelve Data, Yahoo Finance, and CoinGecko. We do not guarantee the accuracy, completeness, or timeliness of third-party data.

This content is designed for UK residents and reflects UK tax rules, thresholds, and legislation. It may not apply to other jurisdictions.

Using this website does not create a professional-client relationship of any kind. MJBurrows is not responsible for any financial loss, damage, or decision made based on the content presented. By using this site, you accept these terms.

This disclaimer may be updated from time to time without prior notice. Last reviewed: 23 April 2026.

MJBurrows is an independent UK personal finance publication, written and edited by Matthew Burrows. There is no parent company, no investor group, and no advertising sales team — decisions about what to cover and how to frame it are made by Matthew alone. Our full Editorial Policy sets out how the site operates in detail.

Commercial model. As of April 2026, MJBurrows generates no revenue. The site carries no display advertising, no affiliate links, no sponsored content, no paid product placements, and no pay-for-coverage arrangements. If this changes in future, it will be disclosed openly on the Editorial Policy page.

Sources. Articles and tools reference primary sources — HM Revenue & Customs (HMRC), gov.uk, the Bank of England, the Office for National Statistics (ONS), the Financial Conduct Authority (FCA), Companies House, and UK government departmental publications (DWP, Treasury). Calculator data uses HMRC-published rates for the 2026/27 tax year. Market data (tickers, asset prices) is provided by Twelve Data, Yahoo Finance, and CoinGecko.

Verification. Every published article is fact-checked before going live. Numerical claims are traced to their primary source, quotes are checked against the original speaker or document, and calculator outputs are tested against HMRC worked examples. See our verification and accuracy policy for the full process.

Corrections. If you spot an error, please report it via the Corrections page. A three-tier severity system commits to specific response times:

- Tier 1 — Urgent (material reader harm, defamatory statements, regulatory or legal issues): acknowledged within 24 hours, page actioned within 24 hours, correction published within 48 hours of confirmation.

- Tier 2 — High (significant factual errors that misinform readers): acknowledged within 3 working days, correction published within 7 working days of confirmation.

- Tier 3 — Standard (minor factual errors, dated references, missing context): acknowledged within 7 working days, correction published at the next regular content review (within the quarter).

Significant corrections are logged on the public Corrections log.

Updates and review cadence. Calculators are reviewed at least quarterly, plus event-driven updates when HMRC publishes new rates (Budget, Autumn Statement, new tax year). Guides are reviewed at least twice a year, with major rewrites whenever underlying regulation changes. Tax-year-sensitive content is prioritised for review at the April tax-year transition.

Get in touch. For editorial enquiries — corrections, story tips, reader questions — the address is contact@mjburrows.com. The contact page is at mjburrows.com/contact. Every email is read personally by Matthew.