£137 billion. That’s how much the UK windfall tax reform could boost the economy by 2050 if Chancellor Rachel Reeves replaces the current energy profits levy with something smarter. But… kicker – without windfall tax changes, Britain’s entire North Sea oil and gas industry might vanish “within years, not decades.”

Offshore Energy UK just released a report that’s somewhat of a financial ultimatum. Reform the UK energy profits levy now, or watch a major industry disappear whilst we’re still heating 85% of British homes with gas.

What’s Wrong with the Current UK Windfall Tax System?

The current UK windfall tax (officially called the energy profits levy) sits at a hefty 38%. It’s supposed to disappear in 2030 (maybe sooner if oil company profits tank), but that timeline might be too little, too late for North Sea energy investment.

OEUK’s CEO David Whitehouse had their say about UK energy taxation: “We’re saying reform the energy profits levy to boost national energy production, investment, unlock 23,000 jobs, and add over £137bn to communities – or keep the tax, gain short-term revenue, and risk the North Sea industry’s collapse.”

That’s not corporate fear-mongering about UK oil and gas taxation. The windfall tax economics back it up.

The Smart Alternative: Profits-Based UK Energy Tax Reform

Instead of a flat windfall tax rate that hammers energy companies regardless of market conditions, OEUK wants a profits-based windfall tax mechanism triggered by “unusually high oil prices.” Think of it as a sliding scale UK energy tax – when oil prices spike, energy company taxes go up. When crude oil prices drop, so do the windfall tax rates.

This UK energy tax approach would let North Sea operators invest with confidence, knowing they won’t get slammed with the same windfall tax rate whether oil’s at $50 or $150 per barrel.

Why UK Windfall Tax Reform Actually Matters for Energy Bills

Here’s the UK energy reality check: Britain needs 10-15 billion barrels of oil and gas to hit net zero goals whilst maintaining energy security. UK energy producers are only lined up for about 4 billion barrels – and even that North Sea production target is now at risk from current windfall tax policy.

What happens when UK domestic energy production drops? We import more oil and gas, energy prices go up, and your household energy bills get uglier. Meanwhile, 23 million British vehicles still run on petrol and diesel, not renewable energy fairy dust and good intentions.

The UK Energy Investment Economic Upside is Massive

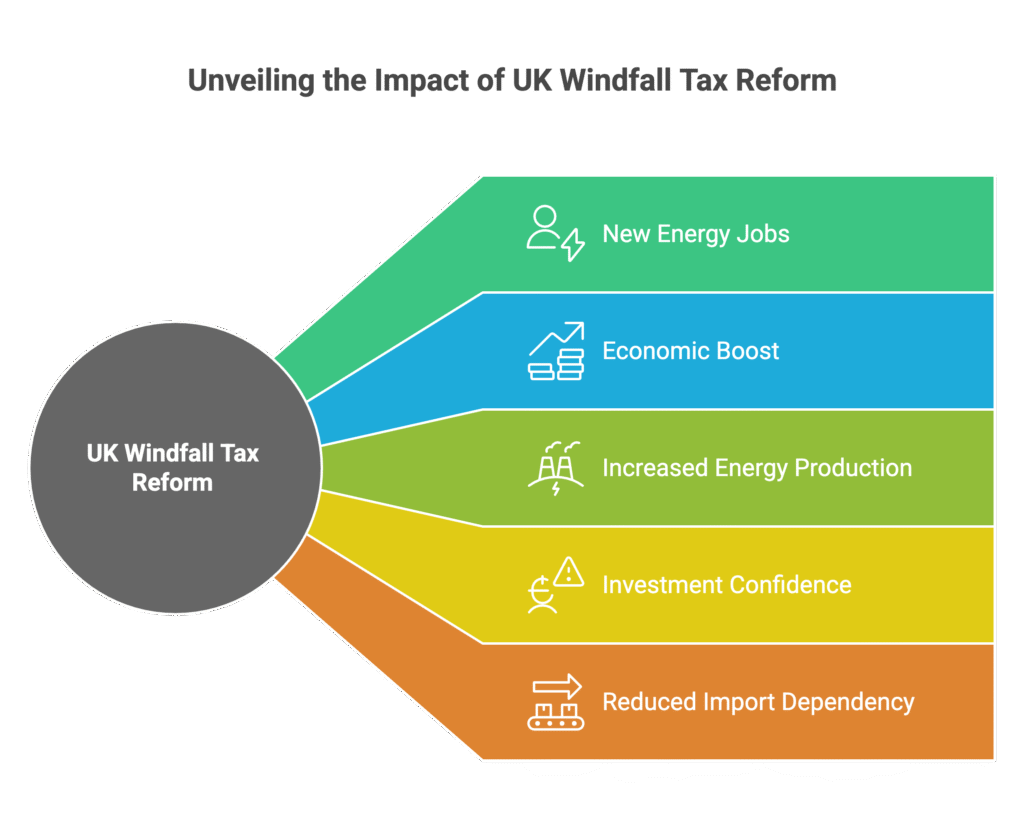

The proposed UK windfall tax reform could unlock:

- 23,000 new UK energy jobs

- £137bn economic boost to UK economy by 2050

- Increased British domestic energy production

- Higher North Sea investment confidence

- Reduced UK energy import dependency

Compare that to the current windfall tax path: short-term government revenue followed by UK energy industry collapse and higher import dependency.

What Happens Next for UK Energy Policy?

The autumn budget is coming, and OEUK is pushing Chancellor Rachel Reeves for “big ideas and ambition” on UK energy taxation. The Treasury hasn’t commented yet on windfall tax reform, but the pressure’s mounting from UK energy sector leaders.

The choice is simple for UK energy future: reform windfall tax now and boost the economy, or stick with the status quo and watch a major British industry disappear whilst energy bills keep climbing.

FAQ: UK Windfall Tax Reform and Energy Policy

Q1: When would the UK windfall tax reform take effect?

A: OEUK wants the energy profits levy replaced next year to save North Sea investment. The current 38% windfall tax is scheduled to end in 2030, but UK energy reform advocates say that’s too late to save the industry.

Q2: How would a profits-based UK windfall tax work?

A: Instead of a flat 38% energy tax rate, windfall tax rates would adjust based on oil and gas market prices. When energy prices spike unusually high, excess oil company profits get taxed more heavily under the reformed windfall tax system.

Q3: What happens if the UK doesn’t reform the windfall tax policy?

A: According to UK energy industry experts, the North Sea oil and gas sector could disappear within years due to current windfall tax levels. This would increase British energy import dependency and likely drive up household energy costs.

Q4: Does UK windfall tax reform conflict with net zero goals?

A: Not according to OEUK energy policy experts. They argue the UK needs 10-15 billion barrels of oil and gas to meet net zero targets whilst transitioning to renewable energy, but domestic producers face windfall tax barriers to achieving even 4 billion barrels.

Q5: What’s the economic impact of UK windfall tax reform?

A: The energy tax reform could generate £137bn for the UK economy by 2050 and create 23,000 British energy jobs. It would also increase domestic energy production and reduce costly energy import dependency.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.

MORE NEWS

Disclosure & Editorial Standards

MJBurrows is not authorised or regulated by the Financial Conduct Authority (FCA). The content on this website — including articles, calculators, and tools — is for general informational and educational purposes only. It does not constitute personal financial, investment, tax, or legal advice and does not take into account your individual circumstances, financial situation, or objectives.

Nothing on this site is a personal recommendation to buy, sell, hold, or otherwise deal in any financial product, asset, or service. You should always conduct your own research and seek advice from a qualified, FCA-regulated financial adviser before making any financial decisions.

Our calculators produce estimates based on simplified models using HMRC-published rates for the current tax year. They cannot account for every individual circumstance and should not be relied upon as exact figures. Tax rules and rates may change — verify current rates with HMRC or a qualified tax adviser.

Projections are not guarantees. Where our tools show future values (investment growth, pension projections, compound interest), these are hypothetical illustrations based on assumed growth rates. Past performance does not guarantee future results. The value of investments can go down as well as up.

Market data displayed on this site is provided by third-party sources including Twelve Data, Yahoo Finance, and CoinGecko. We do not guarantee the accuracy, completeness, or timeliness of third-party data.

This content is designed for UK residents and reflects UK tax rules, thresholds, and legislation. It may not apply to other jurisdictions.

Using this website does not create a professional-client relationship of any kind. MJBurrows is not responsible for any financial loss, damage, or decision made based on the content presented. By using this site, you accept these terms.

This disclaimer may be updated from time to time without prior notice. Last reviewed: 23 April 2026.

MJBurrows is an independent UK personal finance publication, written and edited by Matthew Burrows. There is no parent company, no investor group, and no advertising sales team — decisions about what to cover and how to frame it are made by Matthew alone. Our full Editorial Policy sets out how the site operates in detail.

Commercial model. As of April 2026, MJBurrows generates no revenue. The site carries no display advertising, no affiliate links, no sponsored content, no paid product placements, and no pay-for-coverage arrangements. If this changes in future, it will be disclosed openly on the Editorial Policy page.

Sources. Articles and tools reference primary sources — HM Revenue & Customs (HMRC), gov.uk, the Bank of England, the Office for National Statistics (ONS), the Financial Conduct Authority (FCA), Companies House, and UK government departmental publications (DWP, Treasury). Calculator data uses HMRC-published rates for the 2026/27 tax year. Market data (tickers, asset prices) is provided by Twelve Data, Yahoo Finance, and CoinGecko.

Verification. Every published article is fact-checked before going live. Numerical claims are traced to their primary source, quotes are checked against the original speaker or document, and calculator outputs are tested against HMRC worked examples. See our verification and accuracy policy for the full process.

Corrections. If you spot an error, please report it via the Corrections page. A three-tier severity system commits to specific response times:

- Tier 1 — Urgent (material reader harm, defamatory statements, regulatory or legal issues): acknowledged within 24 hours, page actioned within 24 hours, correction published within 48 hours of confirmation.

- Tier 2 — High (significant factual errors that misinform readers): acknowledged within 3 working days, correction published within 7 working days of confirmation.

- Tier 3 — Standard (minor factual errors, dated references, missing context): acknowledged within 7 working days, correction published at the next regular content review (within the quarter).

Significant corrections are logged on the public Corrections log.

Updates and review cadence. Calculators are reviewed at least quarterly, plus event-driven updates when HMRC publishes new rates (Budget, Autumn Statement, new tax year). Guides are reviewed at least twice a year, with major rewrites whenever underlying regulation changes. Tax-year-sensitive content is prioritised for review at the April tax-year transition.

Get in touch. For editorial enquiries — corrections, story tips, reader questions — the address is contact@mjburrows.com. The contact page is at mjburrows.com/contact. Every email is read personally by Matthew.