UK Debt Crisis Risk: Second Only to France

Here’s a wake-up call: the UK is now the second most likely major economy to face a debt crisis in the next two years. Only France ranks higher. That’s according to a fresh Deutsche Bank survey of financial professionals who aren’t exactly brimming with confidence about Britain’s growth prospects or spending discipline. With borrowing at pandemic-era levels and warnings of a “debt doom loop” from hedge fund legend Ray Dalio, investors are getting nervous. Let’s break down what’s happening and why it matters for your wallet.

France Leads the Pack (and Not in a Good Way)

Over half of institutional investors surveyed by Deutsche Bank flagged France as the most likely candidate for a crisis-level bond sell-off before 2028. Why? Political chaos. The country’s burned through three prime ministers recently, each failing to pass a budget that lawmakers could stomach.

France’s deficit hit 5.8% in 2024—the worst in the G7 except for the US. Former PM François Bayrou stated: France was “heading for bankruptcy.” When your own politicians start using the B-word, you know things are dicey.

UK Takes Silver (Unfortunately)

A fifth of respondents pegged the UK as most vulnerable to a government bond crisis. About half said British debt was the second-riskiest behind France—putting it ahead of both debt-heavy Japan and the US, which is currently running an $1.8 trillion deficit.

That’s not exactly the podium finish anyone wanted.

The UK’s Borrowing Binge

Here’s where it gets uncomfortable: Britain’s taking on debt at pandemic rates—without the pandemic. Since the government’s first Budget in November, yields on 10-year gilts (the main measure of borrowing costs) have jumped over 40 basis points. We’re now at levels not seen since the 2008 financial crisis sent interest rates cratering.

Ray Dalio, founder of Bridgewater Associates and one of the world’s most influential investors, didn’t pull punches. He’s warning the UK is trapped in a “debt doom loop”—a nasty cycle of rising taxes, mounting debt, and stagnant growth.

The Tax-and-Flight Problem

Dalio pointed out something crucial: when conditions worsen, wealthy people leave. And that’s a problem because the top 10% pay roughly 75% of income taxes (similar ratios exist in the UK and US).

“A deterioration in conditions… [has] the effect of causing people with money to leave,” Dalio said. The warning signs are “beginning to flash and flicker.”

Translation? Hike taxes on the rich to fix your debt problem, and they might just pack their bags. That shrinks your tax base, worsens the deficit, and forces more borrowing. Rinse and repeat.

What This Means for You

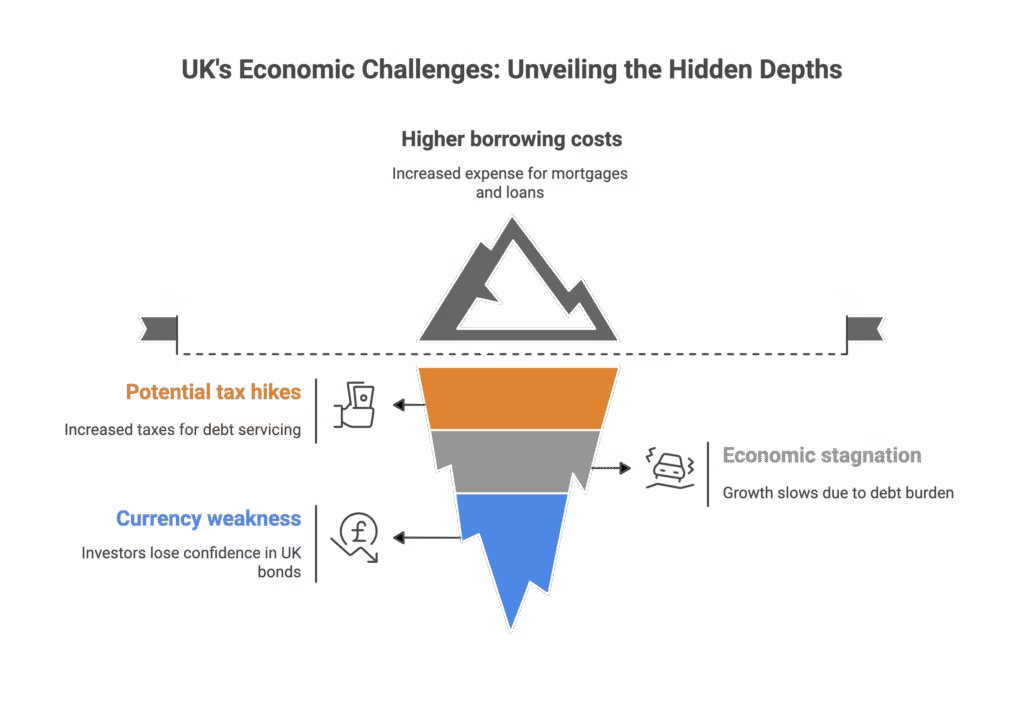

If you’re a UK taxpayer, investor, or business owner, these findings matter. A debt crisis doesn’t happen overnight, but the ingredients are lining up:

- Higher borrowing costs make mortgages and loans more expensive

- Potential tax hikes to service debt could hit middle-income earners too

- Economic stagnation as growth sputters under the weight of debt payments

- Currency weakness if investors lose faith in UK bonds

We’re not at crisis point yet, but the trajectory isn’t great.

The Bottom Line

The UK’s debt situation is raising red flags among people who manage billions. Being second only to France in crisis risk—ahead of Japan and the US—should trigger serious conversations about fiscal discipline and growth strategy.

Whether policymakers can navigate out of this without triggering the doom loop Dalio warns about remains to be seen. One thing’s clear: the borrowing party can’t last forever, and someone’s eventually got to pick up the tab.

Want to track UK debt levels and fiscal policy? Keep an eye on gilt yields and Budget announcements—they’ll tell you where this story’s heading next.

FAQ: UK Debt Crisis Risk

Q1: What exactly is a debt crisis?

A: It’s when investors lose confidence in a government’s ability to repay its debts, triggering a bond sell-off that spikes borrowing costs. This can force spending cuts, tax hikes, or even bailouts—think Greece in 2010.

Q2: Why is France considered more at risk than the UK?

A: France has worse political instability and a larger deficit (5.8% in 2024). Three PMs have resigned recently over budget disputes, and the country lacks a clear fiscal plan.

Q3: What’s a “debt doom loop”?

A: Ray Dalio’s term for a vicious cycle where governments raise taxes to service debt, wealthy people leave, tax revenue falls, deficits grow, and more borrowing is needed. It’s self-reinforcing and hard to escape.

Q4: How does this affect average UK residents?

A: Higher gilt yields mean more expensive mortgages, loans, and credit. Tax hikes may follow to service debt, and sluggish growth could limit wage increases and job opportunities.

Q5: Can the UK avoid a debt crisis?

A: Yes, but it requires discipline: controlling spending, boosting growth, and maintaining investor confidence. The path is narrow, and mistakes could tip things over the edge.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.

MORE NEWS

Disclosure & Editorial Standards

MJBurrows is not authorised or regulated by the Financial Conduct Authority (FCA). The content on this website — including articles, calculators, and tools — is for general informational and educational purposes only. It does not constitute personal financial, investment, tax, or legal advice and does not take into account your individual circumstances, financial situation, or objectives.

Nothing on this site is a personal recommendation to buy, sell, hold, or otherwise deal in any financial product, asset, or service. You should always conduct your own research and seek advice from a qualified, FCA-regulated financial adviser before making any financial decisions.

Our calculators produce estimates based on simplified models using HMRC-published rates for the current tax year. They cannot account for every individual circumstance and should not be relied upon as exact figures. Tax rules and rates may change — verify current rates with HMRC or a qualified tax adviser.

Projections are not guarantees. Where our tools show future values (investment growth, pension projections, compound interest), these are hypothetical illustrations based on assumed growth rates. Past performance does not guarantee future results. The value of investments can go down as well as up.

Market data displayed on this site is provided by third-party sources including Twelve Data, Yahoo Finance, and CoinGecko. We do not guarantee the accuracy, completeness, or timeliness of third-party data.

This content is designed for UK residents and reflects UK tax rules, thresholds, and legislation. It may not apply to other jurisdictions.

Using this website does not create a professional-client relationship of any kind. MJBurrows is not responsible for any financial loss, damage, or decision made based on the content presented. By using this site, you accept these terms.

This disclaimer may be updated from time to time without prior notice. Last reviewed: 23 April 2026.

MJBurrows is an independent UK personal finance publication, written and edited by Matthew Burrows. There is no parent company, no investor group, and no advertising sales team — decisions about what to cover and how to frame it are made by Matthew alone. Our full Editorial Policy sets out how the site operates in detail.

Commercial model. As of April 2026, MJBurrows generates no revenue. The site carries no display advertising, no affiliate links, no sponsored content, no paid product placements, and no pay-for-coverage arrangements. If this changes in future, it will be disclosed openly on the Editorial Policy page.

Sources. Articles and tools reference primary sources — HM Revenue & Customs (HMRC), gov.uk, the Bank of England, the Office for National Statistics (ONS), the Financial Conduct Authority (FCA), Companies House, and UK government departmental publications (DWP, Treasury). Calculator data uses HMRC-published rates for the 2026/27 tax year. Market data (tickers, asset prices) is provided by Twelve Data, Yahoo Finance, and CoinGecko.

Verification. Every published article is fact-checked before going live. Numerical claims are traced to their primary source, quotes are checked against the original speaker or document, and calculator outputs are tested against HMRC worked examples. See our verification and accuracy policy for the full process.

Corrections. If you spot an error, please report it via the Corrections page. A three-tier severity system commits to specific response times:

- Tier 1 — Urgent (material reader harm, defamatory statements, regulatory or legal issues): acknowledged within 24 hours, page actioned within 24 hours, correction published within 48 hours of confirmation.

- Tier 2 — High (significant factual errors that misinform readers): acknowledged within 3 working days, correction published within 7 working days of confirmation.

- Tier 3 — Standard (minor factual errors, dated references, missing context): acknowledged within 7 working days, correction published at the next regular content review (within the quarter).

Significant corrections are logged on the public Corrections log.

Updates and review cadence. Calculators are reviewed at least quarterly, plus event-driven updates when HMRC publishes new rates (Budget, Autumn Statement, new tax year). Guides are reviewed at least twice a year, with major rewrites whenever underlying regulation changes. Tax-year-sensitive content is prioritised for review at the April tax-year transition.

Get in touch. For editorial enquiries — corrections, story tips, reader questions — the address is contact@mjburrows.com. The contact page is at mjburrows.com/contact. Every email is read personally by Matthew.