UK manufacturing PMI plummeted to 47 in August, marking the sector’s worst performance in three months. This downturn signals trouble for Labour’s ambitious manufacturing growth plans as rising costs and declining output threaten the UK’s industrial recovery. With employment falling for ten consecutive months, can UK manufacturing bounce back?

August Manufacturing PMI: Key Numbers Behind the Decline

- PMI: 47 (vs 50 neutral threshold)

- Output: Three-month low

- Employment: 10th consecutive monthly decline

- New Orders: Continued deterioration

The August UK manufacturing data paints a stark picture. S&P Global’s PMI survey reveals manufacturing companies across Britain are struggling with a toxic mix of rising costs and weakening demand for UK manufactured goods.

“August’s final S&P Global UK manufacturing survey provided further signs that the manufacturing sector appears likely to continue to underwhelm,” said EY ITEM Club’s Matt Swannell, highlighting persistent challenges facing UK businesses.

Exports are particularly vulnerable, with trade policy uncertainty dampening international demand for British manufactured products.

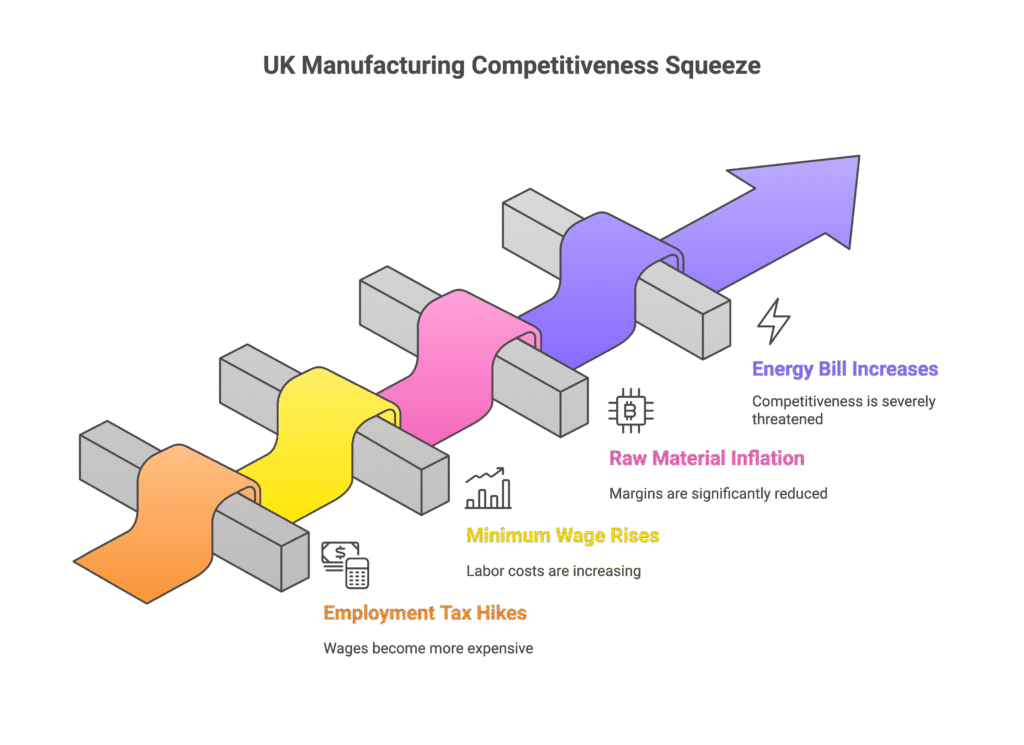

Rachel Reeves Manufacturing Tax Impact: Employment Costs Surge

Rachel Reeves’ Autumn Budget changes are hitting UK manufacturing hard. The Chancellor’s employment tax increases and minimum wage hikes are inflating payroll costs precisely when manufacturing companies need relief.

Key Manufacturing Cost Pressures:

- Employment tax increases affecting manufacturing wages

- Minimum wage rises impacting manufacturing labour costs

- Raw material price inflation squeezing manufacturing margins

- Energy bill increases threatening UK manufacturing competitiveness

Manufacturing redundancies have now persisted for ten months straight—a employment crisis that contradicts Labour’s manufacturing job creation promises. UK firms cite these policy-driven cost increases as major barriers to investment.

Manufacturing business confidence improved marginally in August but remains below historical averages, suggesting CEOs expect continued sector challenges.

UK vs Global Manufacturing: Competitive Disadvantage

While global manufacturing shows mixed signals, UK manufacturing uniquely faces government-imposed cost increases. This policy-driven disadvantage could accelerate job losses and reduce UK market share internationally.

Manufacturing companies planning future operations increasingly worry about:

- Additional tax burdens

- Rising energy costs

- Reduced UK profitability

- Weakened export competitiveness

These sector concerns extend beyond cyclical downturns, suggesting structural challenges within UK manufacturing that require urgent policy intervention.

Make UK Manufacturing Outlook: Strategic Pause or Deeper Problems?

Make UK, the leading UK manufacturing trade body, offers cautious optimism about manufacturing prospects. Senior economist Fhaheen Khan argues current weakness reflects “businesses carefully reviewing their manufacturing growth plans following the government’s industrial strategy announcement.”

This analysis suggests UK companies are strategically repositioning rather than fundamentally declining. However, sustained job losses and falling orders challenge this optimistic narrative.

Manufacturing industry observers remain split on whether this represents temporary adjustment or long-term sector decline requiring comprehensive manufacturing support measures.

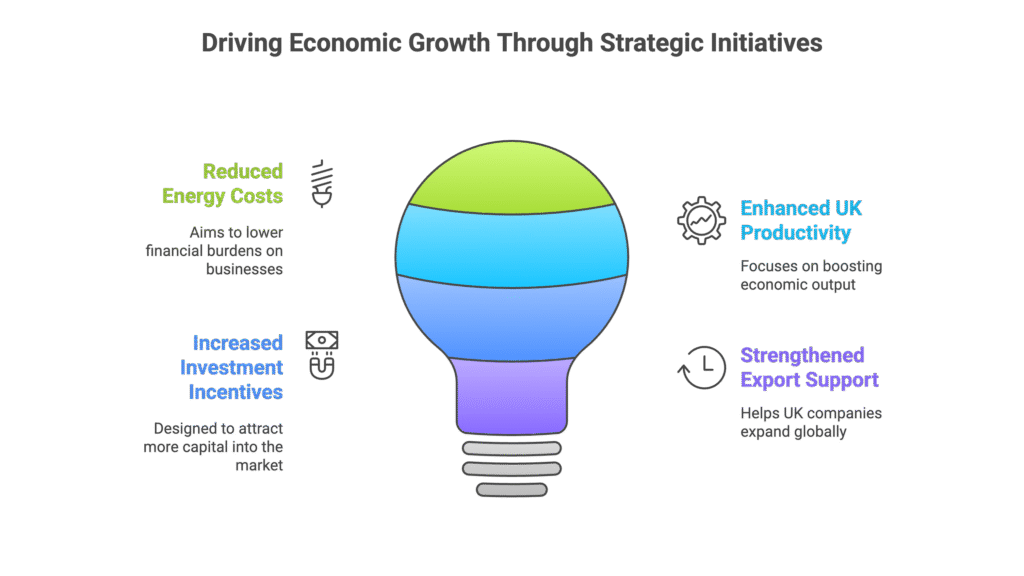

Labour Manufacturing Strategy vs Reality

Labour’s manifesto promised manufacturing renaissance through:

- Reduced energy costs

- Enhanced UK productivity

- Increased investment incentives

- Strengthened export support

However, August’s data reveals growing disconnect between policy promises and sector reality. UK manufacturing needs immediate cost relief, not long-term transformation pledges.

Manufacturing PMI surveys historically underperform official ONS statistics, but ten months of employment decline suggests deeper structural issues than seasonal fluctuations.

UK Manufacturing Recovery: What Manufacturing Companies Need Now

UK manufacturing recovery requires urgent action across multiple policy areas:

Immediate Manufacturing Support:

- Tax relief to offset employment cost increases

- Energy bill assistance for cost-intensive operations

- Export finance to maintain international competitiveness

- Accelerated depreciation allowances

Long-term Manufacturing Strategy:

- Skills development programmes

- Technology investment incentives

- Supply chain resilience measures

- Green transition support

Without decisive intervention, UK manufacturing risks prolonged stagnation that could undermine Britain’s manufacturing base permanently.

The sector’s contribution to UK GDP and employment levels make this downturn a critical economic concern requiring immediate policy response.

UK Manufacturing PMI August 2024: Essential FAQs

Q1: Why did UK manufacturing PMI fall to 47 in August 2024?

A: Multiple manufacturing pressures converged: Rachel Reeves’ employment tax increases inflated manufacturing costs while customer confidence collapsed, reducing orders. Trade uncertainty further damaged manufacturing export prospects, creating perfect storm conditions for UK decline.

Q2: How do UK manufacturing PMI figures compare to official manufacturing data?

A: ONS official manufacturing statistics typically outperform manufacturing PMI surveys by 2-3 points historically. However, manufacturing PMI provides earlier sector insights and captures business sentiment more accurately than retrospective official manufacturing data.

Q3: Will UK manufacturing job losses accelerate beyond August?

A: Manufacturing employment has declined for ten consecutive months, suggesting structural challenges beyond cyclical adjustments. Without manufacturing policy intervention, redundancies could accelerate as companies struggle with unsustainable cost increases.

Q4: Can Labour’s manufacturing strategy reverse UK manufacturing decline?

A: Labour’s manufacturing promises include energy cost reductions and productivity enhancements. However, companies need immediate relief rather than long-term transformation. The manufacturing strategy’s success depends on rapid implementation and cost mitigation measures.

Q5: What makes UK manufacturing less competitive than global manufacturing?

A: UK manufacturing faces unique policy-driven cost increases including employment tax rises and minimum wage hikes. These disadvantages compound existing challenges like high energy costs and post-Brexit trade complications, weakening UK manufacturing competitiveness internationally.

Q6: Which UK manufacturing sectors are worst affected by the PMI decline?

A: While sector-specific manufacturing data wasn’t detailed, industries with high labour costs and energy usage face greatest pressures. Export-dependent manufacturing companies also struggle more with trade uncertainty affecting international demand.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.

MORE NEWS

Disclosure & Editorial Standards

MJBurrows is not authorised or regulated by the Financial Conduct Authority (FCA). The content on this website — including articles, calculators, and tools — is for general informational and educational purposes only. It does not constitute personal financial, investment, tax, or legal advice and does not take into account your individual circumstances, financial situation, or objectives.

Nothing on this site is a personal recommendation to buy, sell, hold, or otherwise deal in any financial product, asset, or service. You should always conduct your own research and seek advice from a qualified, FCA-regulated financial adviser before making any financial decisions.

Our calculators produce estimates based on simplified models using HMRC-published rates for the current tax year. They cannot account for every individual circumstance and should not be relied upon as exact figures. Tax rules and rates may change — verify current rates with HMRC or a qualified tax adviser.

Projections are not guarantees. Where our tools show future values (investment growth, pension projections, compound interest), these are hypothetical illustrations based on assumed growth rates. Past performance does not guarantee future results. The value of investments can go down as well as up.

Market data displayed on this site is provided by third-party sources including Twelve Data, Yahoo Finance, and CoinGecko. We do not guarantee the accuracy, completeness, or timeliness of third-party data.

This content is designed for UK residents and reflects UK tax rules, thresholds, and legislation. It may not apply to other jurisdictions.

Using this website does not create a professional-client relationship of any kind. MJBurrows is not responsible for any financial loss, damage, or decision made based on the content presented. By using this site, you accept these terms.

This disclaimer may be updated from time to time without prior notice. Last reviewed: 23 April 2026.

MJBurrows is an independent UK personal finance publication, written and edited by Matthew Burrows. There is no parent company, no investor group, and no advertising sales team — decisions about what to cover and how to frame it are made by Matthew alone. Our full Editorial Policy sets out how the site operates in detail.

Commercial model. As of April 2026, MJBurrows generates no revenue. The site carries no display advertising, no affiliate links, no sponsored content, no paid product placements, and no pay-for-coverage arrangements. If this changes in future, it will be disclosed openly on the Editorial Policy page.

Sources. Articles and tools reference primary sources — HM Revenue & Customs (HMRC), gov.uk, the Bank of England, the Office for National Statistics (ONS), the Financial Conduct Authority (FCA), Companies House, and UK government departmental publications (DWP, Treasury). Calculator data uses HMRC-published rates for the 2026/27 tax year. Market data (tickers, asset prices) is provided by Twelve Data, Yahoo Finance, and CoinGecko.

Verification. Every published article is fact-checked before going live. Numerical claims are traced to their primary source, quotes are checked against the original speaker or document, and calculator outputs are tested against HMRC worked examples. See our verification and accuracy policy for the full process.

Corrections. If you spot an error, please report it via the Corrections page. A three-tier severity system commits to specific response times:

- Tier 1 — Urgent (material reader harm, defamatory statements, regulatory or legal issues): acknowledged within 24 hours, page actioned within 24 hours, correction published within 48 hours of confirmation.

- Tier 2 — High (significant factual errors that misinform readers): acknowledged within 3 working days, correction published within 7 working days of confirmation.

- Tier 3 — Standard (minor factual errors, dated references, missing context): acknowledged within 7 working days, correction published at the next regular content review (within the quarter).

Significant corrections are logged on the public Corrections log.

Updates and review cadence. Calculators are reviewed at least quarterly, plus event-driven updates when HMRC publishes new rates (Budget, Autumn Statement, new tax year). Guides are reviewed at least twice a year, with major rewrites whenever underlying regulation changes. Tax-year-sensitive content is prioritised for review at the April tax-year transition.

Get in touch. For editorial enquiries — corrections, story tips, reader questions — the address is contact@mjburrows.com. The contact page is at mjburrows.com/contact. Every email is read personally by Matthew.