So, that £40bn tax bombshell Rachel Reeves dropped in her Autumn Budget… UK businesses are still feeling the aftershock. We’re now 10 months into a streak of negative business sentiment that doesn’t look like quitting, according to the latest CBI survey of 900 firms.

While PM Keir Starmer keeps insisting business confidence is bouncing back (citing those rosy Lloyds Bank surveys), the reality on the ground tells a different story. The Confederation of Business Industry data paints a much gloomier picture of ongoing economic uncertainty.

Here’s what you need to know about the ongoing fallout from Reeves’ tax increases and what it means for UK economic growth in 2025.

CBI Survey Shows 10 Months of Business Pessimism After Budget Tax Increases

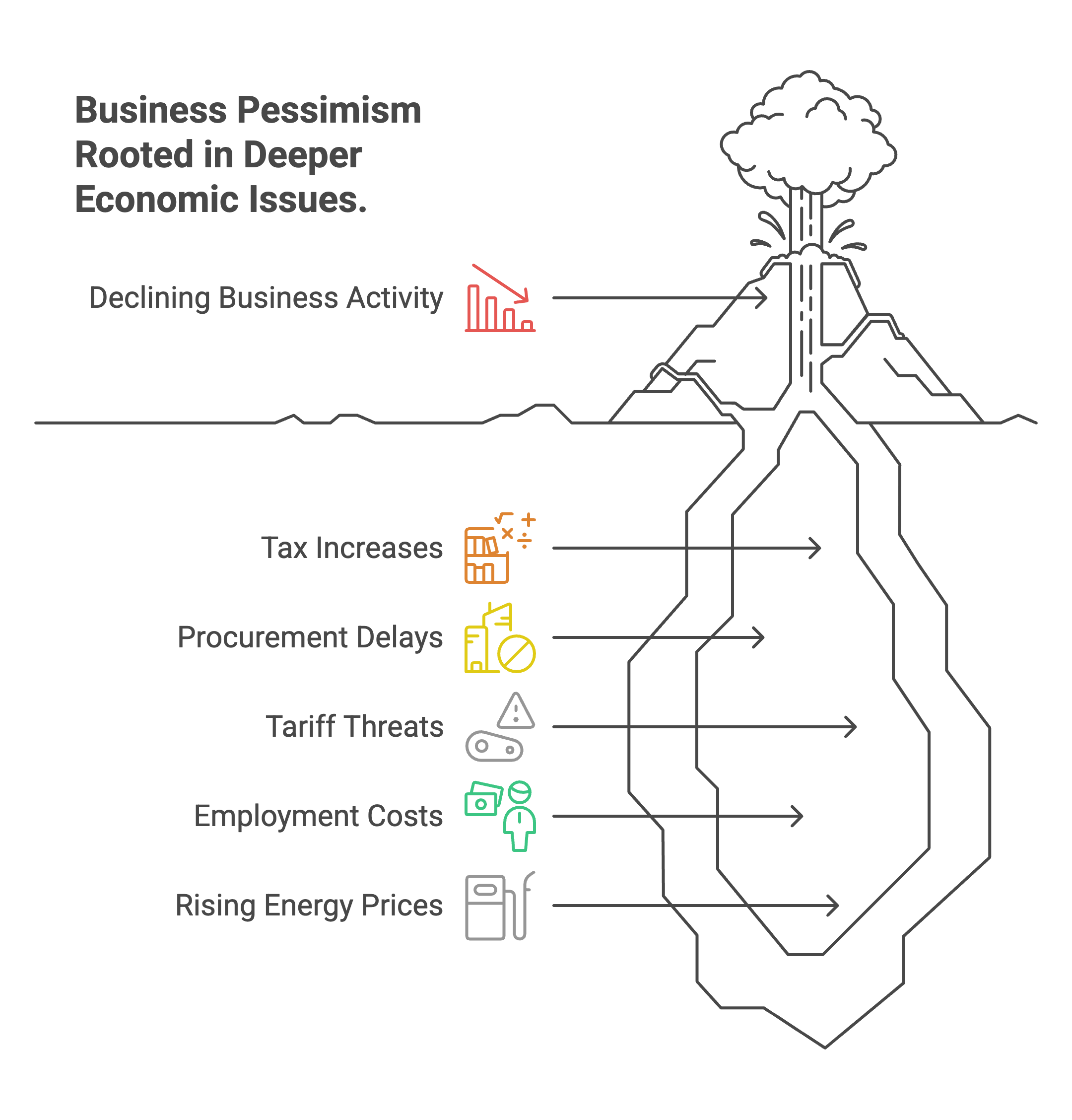

Here’s what’s really happening in boardrooms across Britain. The CBI monthly business sentiment survey shows companies have been planning for declining business activity for 10 straight months. The last time businesses felt optimistic about the next three months? August 2024.

Since then, it’s been downhill. September brought neutral readings at best, and every month after has shown more firms expecting output volumes to drop than those expecting growth.

The main culprits behind persistent negative business sentiment:

- Tax increases from Rachel Reeves’ Autumn Budget

- Delays in public procurement processes

- Tariff threats creating market uncertainty

- Higher employment costs impacting profitability

- Rising energy prices squeezing margins

UK Private Sector Output Declining Faster Than Previous Surveys

The latest CBI economic data reveals private sector output isn’t just declining – it’s dropping at an accelerating pace compared to previous surveys. That’s not exactly the growth trajectory Labour promised for 2025.

“The persistently negative outlook underlines the fragility of demand conditions,” says Alpesh Paleja, CBI deputy chief economist. Translation: businesses are scared, and they’re not spending.

Companies are dealing with a triple whammy of higher employment costs, rising energy prices, and global uncertainty. Their response? Slash costs, cut jobs, and hunker down for what looks like a rough second half of 2025.

The CBI survey data also shows headcount reductions are expected in the three months to October, while selling prices for business services will increase at a slower rate than previous months.

Bank of England Interest Rate Cuts and Services Inflation Trends

The CBI survey shows services inflation cooling off, which could give the Bank of England more room to cut interest rates. Expect a 25 basis point cut to 4% at their next meeting – though don’t expect unanimous agreement among policymakers.

Services inflation decline is crucial because it’s a key price growth indicator that BoE officials monitor closely. Lower services inflation typically signals reduced domestic demand pressure.

But here’s Rachel Reeves’ budget headache: if businesses keep struggling and UK economic growth stalls, her budget headroom gets tighter. That high tax burden she created might be strangling the very growth she needs to balance the books for future budgets.

Defence Sector Emerges as Top UK Growth Investment Opportunity

Want to know where UK investors see opportunity amid economic uncertainty? Defence stocks are topping growth sector predictions, beating out even AI technology investments. A survey of 1,800 investors by trading platform IG suggests defence offers a “more resilient growth story” than tech sectors.

Why defence is outperforming other UK growth sectors:

- Government spending commitments provide stable revenue streams

- Geopolitical tensions create sustained demand

- Conflict threats make defence a defensive investment choice

That could be good news for British defence companies like BAE Systems, Rolls-Royce, and Babcock. Sometimes geopolitical tensions create unexpected UK stock market opportunities.

Impact on Labour’s Growth Mission and Future UK Economic Policy

Ten months after Reeves’ tax raid, UK businesses remain in survival mode. While politicians point to selective surveys showing green shoots, the broader business community sentiment remains pessimistic about future economic conditions.

Key challenges facing Labour’s economic strategy:

- Persistent negative business outlook across all private sectors

- Declining business investment due to tax uncertainty

- Reduced business activity expectations for remainder of 2025

- Employment cost pressures from budget tax changes

The question now: can Labour’s growth mission survive its own tax policy decisions, or will this negative business sentiment become a self-fulfilling prophecy for UK economic performance?

Frequently Asked Questions About UK Business Sentiment and Rachel Reeves’ Budget Impact

Q1: How long has UK business sentiment been negative according to CBI surveys?

A: Business sentiment has been negative for 10 consecutive months according to CBI monthly surveys of 900 firms. The last positive reading for business output expectations was in August 2024, with neutral readings in September followed by persistent negativity.

Q2: What are the main causes of ongoing UK business pessimism in 2025?

A: The primary factors are Rachel Reeves’ tax increases from the Autumn Budget, delays in public procurement, and tariff uncertainty. Additionally, higher employment costs and rising energy prices are weighing heavily on business confidence and investment decisions.

Q3: Will the Bank of England cut interest rates due to declining business activity?

A: Likely yes – expect a 25 basis point cut to 4% at the next BoE meeting. Cooling services inflation from declining business activity gives policymakers more room to stimulate the economy, though the decision may not be unanimous among committee members.

Q4: Which UK sectors are investors most optimistic about despite negative sentiment?

A: Defence tops investment optimism according to an IG survey of 1,800 investors, outranking AI and technology sectors. Investors view defence as offering more resilient growth amid global uncertainties, potentially benefiting companies like BAE Systems and Rolls-Royce.

Q5: How might persistent business negativity affect Rachel Reeves’ future budgets?

A: Ongoing negative business sentiment threatens Labour’s growth mission and could squeeze Reeves’ budget headroom significantly. If economic growth continues stalling due to high tax burdens, she’ll have less fiscal flexibility for future spending or tax adjustments in upcoming budgets.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.

MORE NEWS

Disclosure & Editorial Standards

MJBurrows is not authorised or regulated by the Financial Conduct Authority (FCA). The content on this website — including articles, calculators, and tools — is for general informational and educational purposes only. It does not constitute personal financial, investment, tax, or legal advice and does not take into account your individual circumstances, financial situation, or objectives.

Nothing on this site is a personal recommendation to buy, sell, hold, or otherwise deal in any financial product, asset, or service. You should always conduct your own research and seek advice from a qualified, FCA-regulated financial adviser before making any financial decisions.

Our calculators produce estimates based on simplified models using HMRC-published rates for the current tax year. They cannot account for every individual circumstance and should not be relied upon as exact figures. Tax rules and rates may change — verify current rates with HMRC or a qualified tax adviser.

Projections are not guarantees. Where our tools show future values (investment growth, pension projections, compound interest), these are hypothetical illustrations based on assumed growth rates. Past performance does not guarantee future results. The value of investments can go down as well as up.

Market data displayed on this site is provided by third-party sources including Twelve Data, Yahoo Finance, and CoinGecko. We do not guarantee the accuracy, completeness, or timeliness of third-party data.

This content is designed for UK residents and reflects UK tax rules, thresholds, and legislation. It may not apply to other jurisdictions.

Using this website does not create a professional-client relationship of any kind. MJBurrows is not responsible for any financial loss, damage, or decision made based on the content presented. By using this site, you accept these terms.

This disclaimer may be updated from time to time without prior notice. Last reviewed: 23 April 2026.

MJBurrows is an independent UK personal finance publication, written and edited by Matthew Burrows. There is no parent company, no investor group, and no advertising sales team — decisions about what to cover and how to frame it are made by Matthew alone. Our full Editorial Policy sets out how the site operates in detail.

Commercial model. As of April 2026, MJBurrows generates no revenue. The site carries no display advertising, no affiliate links, no sponsored content, no paid product placements, and no pay-for-coverage arrangements. If this changes in future, it will be disclosed openly on the Editorial Policy page.

Sources. Articles and tools reference primary sources — HM Revenue & Customs (HMRC), gov.uk, the Bank of England, the Office for National Statistics (ONS), the Financial Conduct Authority (FCA), Companies House, and UK government departmental publications (DWP, Treasury). Calculator data uses HMRC-published rates for the 2026/27 tax year. Market data (tickers, asset prices) is provided by Twelve Data, Yahoo Finance, and CoinGecko.

Verification. Every published article is fact-checked before going live. Numerical claims are traced to their primary source, quotes are checked against the original speaker or document, and calculator outputs are tested against HMRC worked examples. See our verification and accuracy policy for the full process.

Corrections. If you spot an error, please report it via the Corrections page. A three-tier severity system commits to specific response times:

- Tier 1 — Urgent (material reader harm, defamatory statements, regulatory or legal issues): acknowledged within 24 hours, page actioned within 24 hours, correction published within 48 hours of confirmation.

- Tier 2 — High (significant factual errors that misinform readers): acknowledged within 3 working days, correction published within 7 working days of confirmation.

- Tier 3 — Standard (minor factual errors, dated references, missing context): acknowledged within 7 working days, correction published at the next regular content review (within the quarter).

Significant corrections are logged on the public Corrections log.

Updates and review cadence. Calculators are reviewed at least quarterly, plus event-driven updates when HMRC publishes new rates (Budget, Autumn Statement, new tax year). Guides are reviewed at least twice a year, with major rewrites whenever underlying regulation changes. Tax-year-sensitive content is prioritised for review at the April tax-year transition.

Get in touch. For editorial enquiries — corrections, story tips, reader questions — the address is contact@mjburrows.com. The contact page is at mjburrows.com/contact. Every email is read personally by Matthew.