Ever wonder what happens when Trump tariffs meet your favourite car brands? Just ask Stellantis shareholders – they’re getting a masterclass in pain right now.

The European automaker behind Vauxhall, Fiat, Alfa Romeo, and a dozen other marques just confirmed Trump’s car tariffs will cost them €1.5bn ($1.4bn) this year, even after the EU-US trade deal cut tariff rates. The Stellantis tariff impact represents one of the largest confirmed hits by a major European car manufacturer since Trump’s trade war escalated.

That’s billion with a ‘b’ – enough to fund several new electric vehicle plants or, you know, keep shareholders from jumping ship. Speaking of which, Stellantis stock tumbled nearly 5% when this tariff news hit the wires.

Stellantis Financial Results: Tariff Damage Report

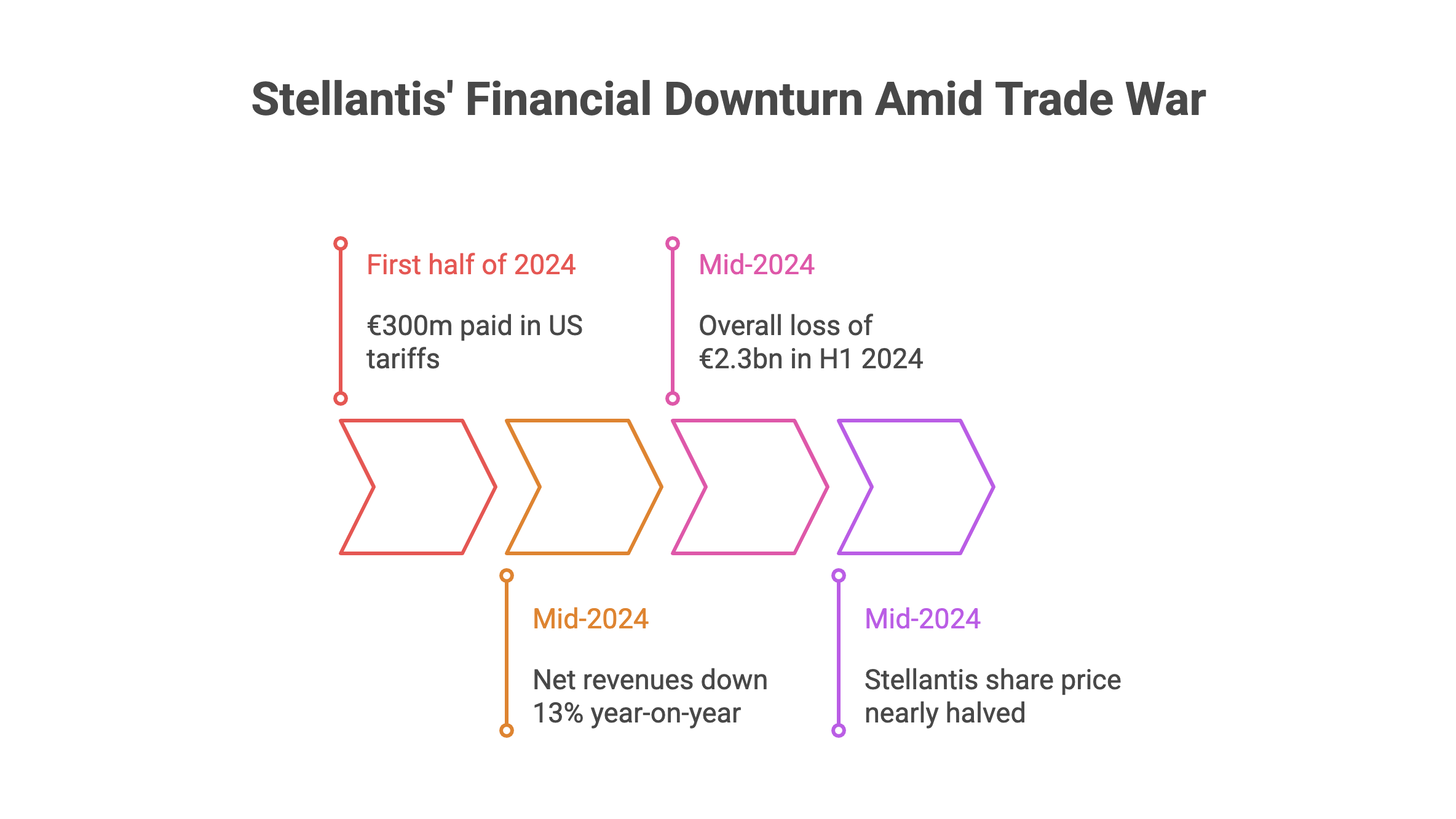

Here’s where the Trump tariffs impact gets ugly fast. Stellantis already paid €300m in US tariffs during the first half of 2024 – and that was before the trade war really escalated.

The Stellantis half-year results read like a financial horror story:

- Net revenues down 13% year-on-year

- Overall loss of €2.3bn in H1 2024

- Stellantis share price nearly halved over the past year

These aren’t just accounting hiccups. This is what happens when Chinese EV competitors flood European markets whilst you’re still figuring out how to make electric cars people actually want to buy.

EU-US Trade Deal 2025: Limited Relief from Trump Tariffs

Sunday’s EU-US trade agreement was supposed to be the cavalry riding over the hill for European automakers. Instead, it feels more like negotiating down from a mugging to a pickpocketing.

The “victory”? EU car tariffs capped at 15% instead of the threatened 30% Trump tariff rates. The price? Europe promised billions in investments into US energy and defence sectors – basically paying protection money with extra steps.

French PM François Bayrou didn’t seem best pleased, calling the EU-US deal a “submission” and a “dark day” for European trade. German Chancellor Friedrich Merz was slightly more diplomatic but equally pessimistic, warning of “considerable damage” to Germany’s export-heavy automotive industry.

Stellantis CEO Strategy: Navigating Automotive Industry Challenges

New Stellantis CEO Antonio Filosa inherited this mess when he took over in May, after his predecessor Carlos Tavares abruptly resigned over “different views” with the board. (Translation: the board wanted results, Tavares couldn’t deliver the automotive turnaround.)

Filosa’s playing it straight: “Our new leadership team, while realistic about the challenges, will continue making the tough decisions needed to re-establish profitable growth.”

That’s CEO-speak for “buckle up, it’s going to get worse before it gets better.”

The European automaker expects revenue and cash flow to recover, but when you’re competing against cheap Chinese EVs whilst paying Trump tariffs, that’s quite the uphill battle for any automotive company.

Stellantis Stock Impact: What Investors Need to Know

If you’re eyeing a new Vauxhall or Alfa, expect car prices to climb. Automotive companies don’t eat billion-dollar tariff bills – they pass Trump tariff costs along to consumers.

For investors, Stellantis stock represents the broader challenge facing European automakers: caught between aggressive Chinese EV competition and protectionist American trade policies, whilst trying to navigate the electric vehicle transition without going broke.

The next few quarters will show whether Filosa’s automotive industry strategy can turn this ship around or if Stellantis becomes another casualty of the global trade war.

FAQ

Q1: Why is Stellantis being hit so hard by Trump tariffs?

A: The automaker exports significant volumes from European plants to the US car market. Trump’s automotive tariffs specifically target these imports, making Stellantis vehicles more expensive for American consumers and eating into profit margins.

Q2: Will the EU-US trade deal actually help Stellantis tariff costs?

A: Marginally. The 15% tariff rate is better than the threatened 30% Trump tariffs, but it’s still a massive cost burden. The €1.5bn Stellantis tariff hit shows even the “reduced” rates are devastating for European car manufacturers.

Q3: How does this Stellantis tariff impact compare to other automakers?

A: Stellantis is the first major European automotive company to provide specific Trump tariff guidance post-EU deal. Other car exporters are likely facing similar trade war pressures but haven’t disclosed exact financial figures yet.

Q4: What’s driving Stellantis’s broader struggles beyond tariff costs?

A: The automotive giant is getting squeezed by cheap Chinese EV competitors in key markets whilst struggling to update its own electric vehicle lineup fast enough. It’s a classic case of being caught in the middle during an industry transition.

Q5: Should investors buy the dip on Stellantis stock after tariff news?

A: That depends on your risk tolerance and belief in the new CEO’s automotive turnaround plan. The fundamentals are challenging, but Stellantis shares have already been hammered pretty hard. Do your own research and consider the broader car industry trends.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.

MORE NEWS

Disclosure & Editorial Standards

MJBurrows is not authorised or regulated by the Financial Conduct Authority (FCA). The content on this website — including articles, calculators, and tools — is for general informational and educational purposes only. It does not constitute personal financial, investment, tax, or legal advice and does not take into account your individual circumstances, financial situation, or objectives.

Nothing on this site is a personal recommendation to buy, sell, hold, or otherwise deal in any financial product, asset, or service. You should always conduct your own research and seek advice from a qualified, FCA-regulated financial adviser before making any financial decisions.

Our calculators produce estimates based on simplified models using HMRC-published rates for the current tax year. They cannot account for every individual circumstance and should not be relied upon as exact figures. Tax rules and rates may change — verify current rates with HMRC or a qualified tax adviser.

Projections are not guarantees. Where our tools show future values (investment growth, pension projections, compound interest), these are hypothetical illustrations based on assumed growth rates. Past performance does not guarantee future results. The value of investments can go down as well as up.

Market data displayed on this site is provided by third-party sources including Twelve Data, Yahoo Finance, and CoinGecko. We do not guarantee the accuracy, completeness, or timeliness of third-party data.

This content is designed for UK residents and reflects UK tax rules, thresholds, and legislation. It may not apply to other jurisdictions.

Using this website does not create a professional-client relationship of any kind. MJBurrows is not responsible for any financial loss, damage, or decision made based on the content presented. By using this site, you accept these terms.

This disclaimer may be updated from time to time without prior notice. Last reviewed: 23 April 2026.

MJBurrows is an independent UK personal finance publication, written and edited by Matthew Burrows. There is no parent company, no investor group, and no advertising sales team — decisions about what to cover and how to frame it are made by Matthew alone. Our full Editorial Policy sets out how the site operates in detail.

Commercial model. As of April 2026, MJBurrows generates no revenue. The site carries no display advertising, no affiliate links, no sponsored content, no paid product placements, and no pay-for-coverage arrangements. If this changes in future, it will be disclosed openly on the Editorial Policy page.

Sources. Articles and tools reference primary sources — HM Revenue & Customs (HMRC), gov.uk, the Bank of England, the Office for National Statistics (ONS), the Financial Conduct Authority (FCA), Companies House, and UK government departmental publications (DWP, Treasury). Calculator data uses HMRC-published rates for the 2026/27 tax year. Market data (tickers, asset prices) is provided by Twelve Data, Yahoo Finance, and CoinGecko.

Verification. Every published article is fact-checked before going live. Numerical claims are traced to their primary source, quotes are checked against the original speaker or document, and calculator outputs are tested against HMRC worked examples. See our verification and accuracy policy for the full process.

Corrections. If you spot an error, please report it via the Corrections page. A three-tier severity system commits to specific response times:

- Tier 1 — Urgent (material reader harm, defamatory statements, regulatory or legal issues): acknowledged within 24 hours, page actioned within 24 hours, correction published within 48 hours of confirmation.

- Tier 2 — High (significant factual errors that misinform readers): acknowledged within 3 working days, correction published within 7 working days of confirmation.

- Tier 3 — Standard (minor factual errors, dated references, missing context): acknowledged within 7 working days, correction published at the next regular content review (within the quarter).

Significant corrections are logged on the public Corrections log.

Updates and review cadence. Calculators are reviewed at least quarterly, plus event-driven updates when HMRC publishes new rates (Budget, Autumn Statement, new tax year). Guides are reviewed at least twice a year, with major rewrites whenever underlying regulation changes. Tax-year-sensitive content is prioritised for review at the April tax-year transition.

Get in touch. For editorial enquiries — corrections, story tips, reader questions — the address is contact@mjburrows.com. The contact page is at mjburrows.com/contact. Every email is read personally by Matthew.