Stablecoin payments just got a massive boost. Mastercard and Circle announced on Tuesday that acquiring banks across Eastern Europe, the Middle East, and Africa can now settle transactions using USDC and EURC stablecoins—marking the first time the EEMEA region can access instant digital settlements at scale.

This isn’t just another crypto experiment. With stablecoins processing $27.6 trillion in transactions during 2024, surpassing Visa and Mastercard’s combined volumes, the payment giant is making a strategic play to stay ahead of the digital currency revolution. Here’s what this means for businesses across EEMEA and why stablecoin adoption is accelerating globally.

Mastercard USDC Settlement: What’s Actually Happening

The expanded Mastercard Circle partnership allows acquiring banks in the EEMEA region to settle merchant payments instantly using Circle’s USDC (USD Coin) and EURC (Euro Coin) stablecoins. Arab Financial Services and Eazy Financial Services became the first institutions to implement this stablecoin settlement capability, setting the stage for widespread adoption.

Think of acquiring banks as the crucial middlemen who connect your local businesses to Mastercard’s payment network. Now, instead of waiting days for traditional banking settlements, they can receive payments in regulated stablecoins that clear instantly.

“This is a key move for Mastercard. Our strategic goal is to integrate stablecoins into the financial mainstream by investing in the infrastructure, governance, and partnerships to support this exciting payment evolution from fiat to tokenised and programmable money,” said Dimitrios Dosis, Mastercard’s president for EEMEA.

Why USDC and EURC Beat Traditional Cross-Border Payments

Traditional international payments are painfully slow and expensive. Stablecoin transaction volumes grew from $560 billion in 2020 to $5.7 trillion in 2024, largely because they solve real problems that legacy systems can’t touch.

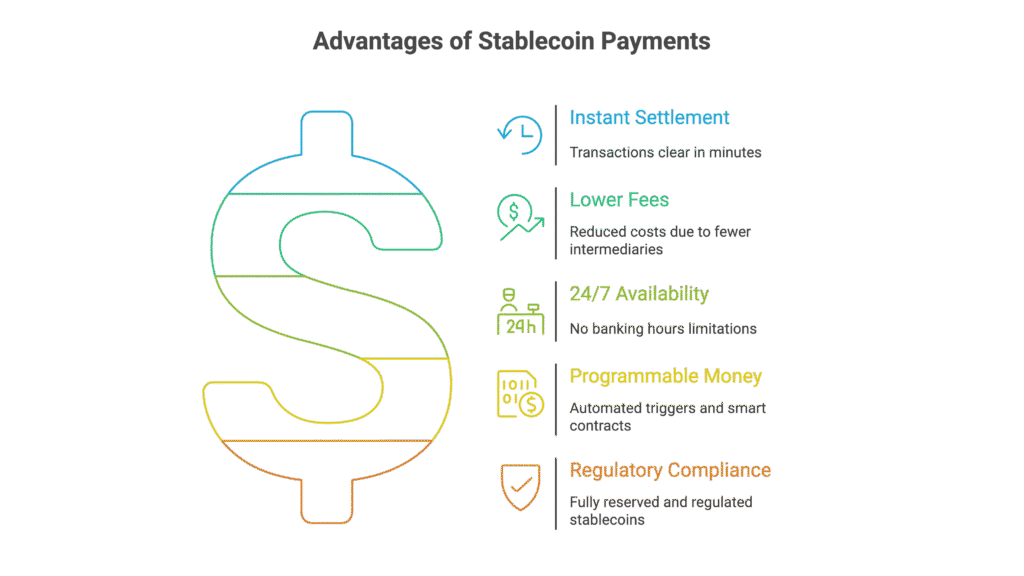

Key advantages of stablecoin payments:

- Instant settlement: USDC transactions clear in minutes, not 2-5 business days

- Lower fees: Fewer intermediaries mean significantly reduced costs

- 24/7 availability: No banking hours limitations

- Programmable money: Automated triggers and smart contract functionality

- Regulatory compliance: Fully reserved and regulated stablecoins

Circle’s Chief Business Officer Kash Razzaghi explained: “Our expanded partnership with Mastercard will enable wider reach, global access, and scaled impact, so that USDC can become as ubiquitous as traditional payments.”

EEMEA Region Gets First-Mover Advantage in Digital Payments

The EEMEA expansion represents more than geographic growth—it’s strategic positioning in emerging markets where traditional banking infrastructure often struggles with cross-border efficiency.

Arab Financial Services CEO Samer Soliman noted that USDC settlements provide enhanced liquidity and operational efficiency, reducing friction in high-volume transactions. For businesses operating across multiple currencies and borders, this could dramatically streamline operations.

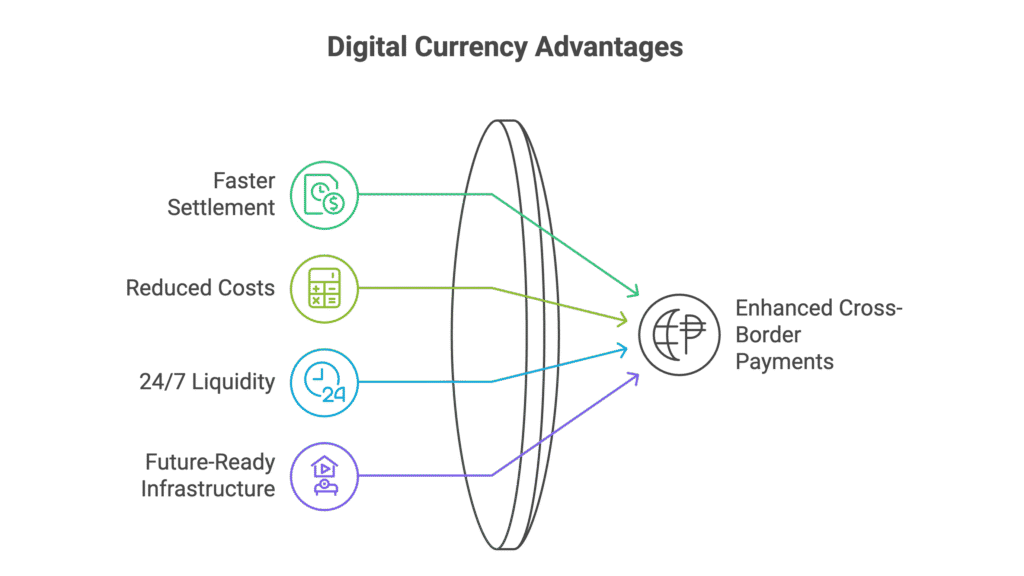

Real-world impact for EEMEA businesses:

- Merchants receive faster settlement in preferred digital currencies

- Reduced forex conversion costs and delays

- Access to 24/7 liquidity without traditional banking constraints

- Future-ready infrastructure aligned with digital asset adoption

Mastercard’s Broader Stablecoin Strategy Beyond Circle

This Circle partnership fits into Mastercard’s aggressive stablecoin expansion. The company tokenized 30% of its transactions in 2024, while supporting multiple regulated stablecoins including Paxos’ USDG, Fise FIUSD, and PayPal’s PYUSD.

Following regulatory clarity from the GENIUS Act, Mastercard announced new capabilities through Mastercard Move and its Multi-Token Network to integrate stablecoins into mainstream financial systems. The company isn’t just adapting to crypto—it’s building the infrastructure to dominate digital payments.

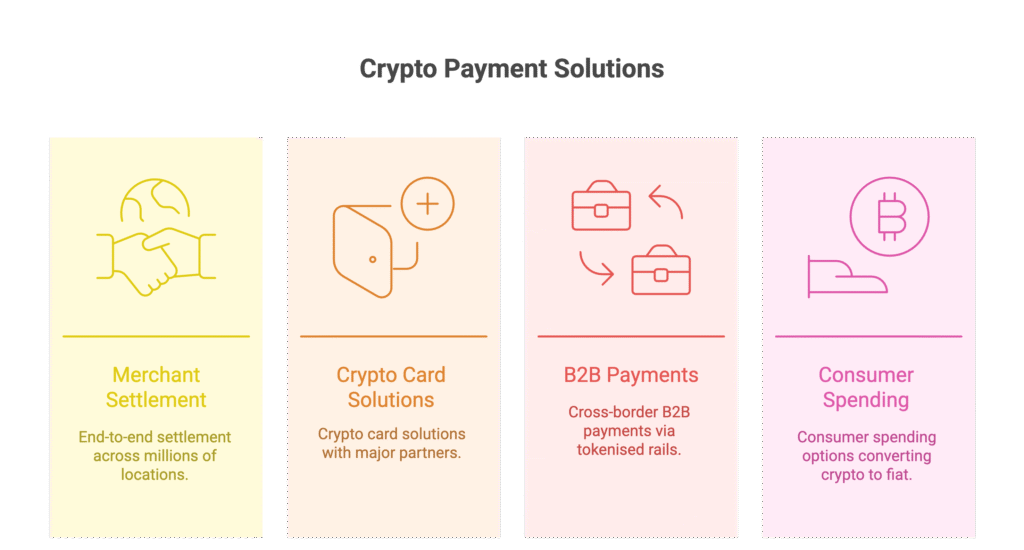

Mastercard’s stablecoin ecosystem includes:

- End-to-end settlement capabilities across 150+ million merchant locations

- Crypto card solutions with partners like MetaMask, Kraken, and Binance

- Cross-border B2B payment solutions through tokenised rails

- Consumer spending options that seamlessly convert crypto to fiat

Market Impact: Stablecoins Challenge Traditional Payment Networks

The numbers tell the story. Payment processing fees for merchants totalled a record $187.2 billion in 2024, creating enormous pressure for more efficient alternatives. Circle’s USDC emerged as the dominant stablecoin for on-chain transactions, accounting for 70% of total transfer volume.

Even traditional competitors acknowledge the shift. While Mastercard’s Chief Product Officer noted that 90% of current stablecoin volume serves crypto trading rather than general payments, the trend toward practical utility is accelerating rapidly.

Recent research shows 88% of executives across payments, compliance and treasury functions say regulation is no longer a barrier to using stablecoin payments, with 49% already using stablecoins operationally.

What’s Next for Stablecoin Adoption in 2025

The Mastercard Circle EEMEA expansion signals broader institutional acceptance. With partnerships spanning JPMorgan Chase, Standard Chartered, and major crypto exchanges, Mastercard is building comprehensive stablecoin infrastructure that extends far beyond simple payment processing.

For businesses in Eastern Europe, the Middle East, and Africa, this represents immediate access to next-generation payment technology without waiting for local banking system upgrades. The question isn’t whether stablecoin payments will expand—it’s how quickly traditional businesses will adapt.

Ready to explore how stablecoin settlements could streamline your cross-border operations? The infrastructure is now live, and early adopters are already seeing operational benefits.

Frequently Asked Questions About Mastercard USDC Settlement

Q1: Which regions can now access Mastercard stablecoin settlement services?

A: The expanded partnership covers Eastern Europe, the Middle East, and Africa (EEMEA). Arab Financial Services and Eazy Financial Services are the first acquiring banks offering USDC and EURC settlement in these regions.

Q2: How do USDC settlements compare to traditional banking for merchants?

A: USDC settlements clear instantly versus 2-5 business days for traditional cross-border transfers. They also typically involve lower fees and 24/7 availability, plus programmable functionality for automated business processes.

Q3: What makes USDC and EURC different from other cryptocurrencies for payments?

A: USDC and EURC are regulated stablecoins backed by fully reserved assets, making their value stable and predictable. Unlike volatile cryptocurrencies, they’re designed specifically for payments and maintain consistent value pegged to the US dollar and euro respectively.

Q4: Will this affect regular consumer payments using Mastercard?

A: Initially, this focuses on merchant settlement rather than consumer transactions. However, it creates infrastructure that could enable faster, cheaper international payments for consumers over time as the technology scales.

Q5: What regulatory frameworks support this stablecoin expansion?

A: The partnership builds on regulatory clarity from the US GENIUS Act and similar frameworks in the EU, UAE, and other regions that provide oversight for stablecoin operations while enabling innovation in digital payments.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.

MORE NEWS

Disclosure & Editorial Standards

MJBurrows is not authorised or regulated by the Financial Conduct Authority (FCA). The content on this website — including articles, calculators, and tools — is for general informational and educational purposes only. It does not constitute personal financial, investment, tax, or legal advice and does not take into account your individual circumstances, financial situation, or objectives.

Nothing on this site is a personal recommendation to buy, sell, hold, or otherwise deal in any financial product, asset, or service. You should always conduct your own research and seek advice from a qualified, FCA-regulated financial adviser before making any financial decisions.

Our calculators produce estimates based on simplified models using HMRC-published rates for the current tax year. They cannot account for every individual circumstance and should not be relied upon as exact figures. Tax rules and rates may change — verify current rates with HMRC or a qualified tax adviser.

Projections are not guarantees. Where our tools show future values (investment growth, pension projections, compound interest), these are hypothetical illustrations based on assumed growth rates. Past performance does not guarantee future results. The value of investments can go down as well as up.

Market data displayed on this site is provided by third-party sources including Twelve Data, Yahoo Finance, and CoinGecko. We do not guarantee the accuracy, completeness, or timeliness of third-party data.

This content is designed for UK residents and reflects UK tax rules, thresholds, and legislation. It may not apply to other jurisdictions.

Using this website does not create a professional-client relationship of any kind. MJBurrows is not responsible for any financial loss, damage, or decision made based on the content presented. By using this site, you accept these terms.

This disclaimer may be updated from time to time without prior notice. Last reviewed: 23 April 2026.

MJBurrows is an independent UK personal finance publication, written and edited by Matthew Burrows. There is no parent company, no investor group, and no advertising sales team — decisions about what to cover and how to frame it are made by Matthew alone. Our full Editorial Policy sets out how the site operates in detail.

Commercial model. As of April 2026, MJBurrows generates no revenue. The site carries no display advertising, no affiliate links, no sponsored content, no paid product placements, and no pay-for-coverage arrangements. If this changes in future, it will be disclosed openly on the Editorial Policy page.

Sources. Articles and tools reference primary sources — HM Revenue & Customs (HMRC), gov.uk, the Bank of England, the Office for National Statistics (ONS), the Financial Conduct Authority (FCA), Companies House, and UK government departmental publications (DWP, Treasury). Calculator data uses HMRC-published rates for the 2026/27 tax year. Market data (tickers, asset prices) is provided by Twelve Data, Yahoo Finance, and CoinGecko.

Verification. Every published article is fact-checked before going live. Numerical claims are traced to their primary source, quotes are checked against the original speaker or document, and calculator outputs are tested against HMRC worked examples. See our verification and accuracy policy for the full process.

Corrections. If you spot an error, please report it via the Corrections page. A three-tier severity system commits to specific response times:

- Tier 1 — Urgent (material reader harm, defamatory statements, regulatory or legal issues): acknowledged within 24 hours, page actioned within 24 hours, correction published within 48 hours of confirmation.

- Tier 2 — High (significant factual errors that misinform readers): acknowledged within 3 working days, correction published within 7 working days of confirmation.

- Tier 3 — Standard (minor factual errors, dated references, missing context): acknowledged within 7 working days, correction published at the next regular content review (within the quarter).

Significant corrections are logged on the public Corrections log.

Updates and review cadence. Calculators are reviewed at least quarterly, plus event-driven updates when HMRC publishes new rates (Budget, Autumn Statement, new tax year). Guides are reviewed at least twice a year, with major rewrites whenever underlying regulation changes. Tax-year-sensitive content is prioritised for review at the April tax-year transition.

Get in touch. For editorial enquiries — corrections, story tips, reader questions — the address is contact@mjburrows.com. The contact page is at mjburrows.com/contact. Every email is read personally by Matthew.