Picture this: you’ve got £50K in Bitcoin but need cash for a house deposit. Instead of selling your crypto (and triggering taxes), you simply borrow against it. That’s the future Bitwise CEO Hunter Horsley says is arriving within 6-12 months.

Crypto credit markets are positioned for explosive growth, with the potential to unlock trillions in capital that’s currently sitting idle. The lending boom could transform how we think about money, investing, and accessing liquidity without liquidising assets.

The $64 Trillion Opportunity

Horsley dropped some numbers on X that’ll make your head spin. There’s nearly $4 trillion in crypto assets currently locked up, waiting to be borrowed against. Add in $60 trillion in U.S. public equities that could be tokenized, and you’ve got a massive untapped lending market.

“When people can borrow against this crypto, rather than sell, they will,” Horsley explained. Makes sense – why liquidise appreciating assets when you could just use them as collateral?

Why Small Investors Win Big

Here’s the game-changer: tokenised lending opens credit markets to everyone. Right now, if you own $7,000 worth of Apple stock, you can’t do much except sell or hold. But once that stock gets tokenised on-chain? Suddenly you can borrow against it for the first time.

Your portfolio becomes your personal ATM, accessible 24/7.

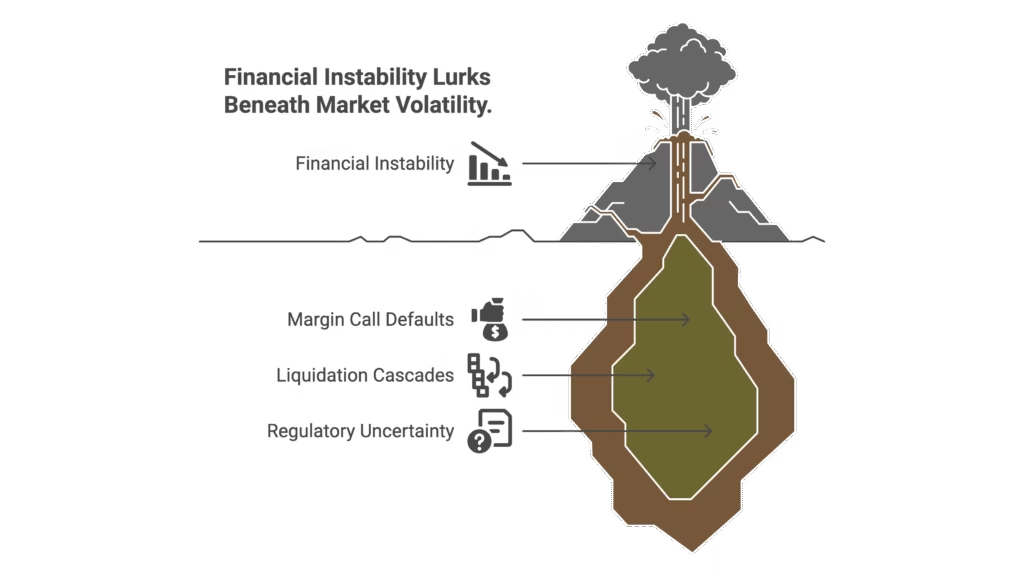

The Risks Worth Watching

Naturally, crypto lending isn’t risk-free. We’ve seen what happens when leverage meets volatility (Terra Luna, FTX, anyone?).

Key Concerns Include:

- Over-leveraging in volatile markets

- Liquidation cascades during crashes

- Regulatory uncertainty around tokenised assets

But proponents argue that proper risk management could make these systems more robust than traditional credit markets.

What This Means for Your Money

If Horsley’s right, we’re looking at a fundamental shift in capital markets. Instead of choosing between holding assets and accessing liquidity, you get both. This could be huge for retail investors wanting cash flow while staying invested, institutions seeking new yield opportunities, and global markets needing more efficient capital allocation.

The credit revolution isn’t just coming – it’s already building momentum. Smart money is paying attention.

FAQ: Crypto Credit Markets Explained

Q1: How soon could mainstream crypto lending actually happen?

A: According to Horsley, significant growth could start in 6-12 months. The infrastructure is already being built by major DeFi platforms and traditional finance players entering the space.

Q2: What’s the difference between crypto lending and traditional bank loans?

A: Crypto lending is typically over-collateralised and happens on-chain without credit checks. Traditional loans rely on credit scores and are usually under-collateralised.

Q3: Is borrowing against crypto actually safe?

A: It depends on the platform, collateral ratios, and market conditions. The risk of liquidation is real if your collateral drops in value.

Q4: Could tokenised stock lending replace traditional margin accounts?

A: Potentially, yes. Tokenised assets could offer 24/7 access, lower fees, and more flexible terms than traditional brokers.

Q5: What happens if the crypto market crashes while I have loans out?

A: You could face liquidation if your collateral falls below required ratios. Most platforms have safeguards, but crashes can trigger rapid liquidations.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.

MORE NEWS

Disclosure & Editorial Standards

MJBurrows is not authorised or regulated by the Financial Conduct Authority (FCA). The content on this website — including articles, calculators, and tools — is for general informational and educational purposes only. It does not constitute personal financial, investment, tax, or legal advice and does not take into account your individual circumstances, financial situation, or objectives.

Nothing on this site is a personal recommendation to buy, sell, hold, or otherwise deal in any financial product, asset, or service. You should always conduct your own research and seek advice from a qualified, FCA-regulated financial adviser before making any financial decisions.

Our calculators produce estimates based on simplified models using HMRC-published rates for the current tax year. They cannot account for every individual circumstance and should not be relied upon as exact figures. Tax rules and rates may change — verify current rates with HMRC or a qualified tax adviser.

Projections are not guarantees. Where our tools show future values (investment growth, pension projections, compound interest), these are hypothetical illustrations based on assumed growth rates. Past performance does not guarantee future results. The value of investments can go down as well as up.

Market data displayed on this site is provided by third-party sources including Twelve Data, Yahoo Finance, and CoinGecko. We do not guarantee the accuracy, completeness, or timeliness of third-party data.

This content is designed for UK residents and reflects UK tax rules, thresholds, and legislation. It may not apply to other jurisdictions.

Using this website does not create a professional-client relationship of any kind. MJBurrows is not responsible for any financial loss, damage, or decision made based on the content presented. By using this site, you accept these terms.

This disclaimer may be updated from time to time without prior notice. Last reviewed: 23 April 2026.

MJBurrows is an independent UK personal finance publication, written and edited by Matthew Burrows. There is no parent company, no investor group, and no advertising sales team — decisions about what to cover and how to frame it are made by Matthew alone. Our full Editorial Policy sets out how the site operates in detail.

Commercial model. As of April 2026, MJBurrows generates no revenue. The site carries no display advertising, no affiliate links, no sponsored content, no paid product placements, and no pay-for-coverage arrangements. If this changes in future, it will be disclosed openly on the Editorial Policy page.

Sources. Articles and tools reference primary sources — HM Revenue & Customs (HMRC), gov.uk, the Bank of England, the Office for National Statistics (ONS), the Financial Conduct Authority (FCA), Companies House, and UK government departmental publications (DWP, Treasury). Calculator data uses HMRC-published rates for the 2026/27 tax year. Market data (tickers, asset prices) is provided by Twelve Data, Yahoo Finance, and CoinGecko.

Verification. Every published article is fact-checked before going live. Numerical claims are traced to their primary source, quotes are checked against the original speaker or document, and calculator outputs are tested against HMRC worked examples. See our verification and accuracy policy for the full process.

Corrections. If you spot an error, please report it via the Corrections page. A three-tier severity system commits to specific response times:

- Tier 1 — Urgent (material reader harm, defamatory statements, regulatory or legal issues): acknowledged within 24 hours, page actioned within 24 hours, correction published within 48 hours of confirmation.

- Tier 2 — High (significant factual errors that misinform readers): acknowledged within 3 working days, correction published within 7 working days of confirmation.

- Tier 3 — Standard (minor factual errors, dated references, missing context): acknowledged within 7 working days, correction published at the next regular content review (within the quarter).

Significant corrections are logged on the public Corrections log.

Updates and review cadence. Calculators are reviewed at least quarterly, plus event-driven updates when HMRC publishes new rates (Budget, Autumn Statement, new tax year). Guides are reviewed at least twice a year, with major rewrites whenever underlying regulation changes. Tax-year-sensitive content is prioritised for review at the April tax-year transition.

Get in touch. For editorial enquiries — corrections, story tips, reader questions — the address is contact@mjburrows.com. The contact page is at mjburrows.com/contact. Every email is read personally by Matthew.