BP shares jumped nearly 2% to 413.84p in early Tuesday trading, defying expectations after the British oil major reported a 14% decline in second-quarter profits. The FTSE 100 energy giant watched Q2 2025 earnings fall to $2.4 billion, yet somehow convinced investors to pile in. How? By launching a $750 million share buyback programme and increasing dividends — proving that sometimes cash talks louder than earnings.

The London-based BP plc posted $95.6 billion in total revenue for H1 2025 — down 2.7% year-over-year — whilst profit before tax barely moved from $5.9 billion to $6 billion. But, despite weaker oil prices and lower trading performance, the company boosted its dividend by 4% to 8.32 cents per share. Sometimes the best defence is a good offence in the volatile energy sector.

Oil Prices 2025: Volatile Brent Crude Impacts BP Earnings

The first half of 2025 saw extreme oil price volatility that directly impacted BP’s financial performance. Brent crude oil prices crashed to four-year lows in April, hitting $59.23 per barrel after President Trump imposed sweeping tariffs on US trading partners, sparking global trade war fears. Then June brought dramatic reversal — Israel’s strikes on Iran’s nuclear facilities sent oil prices soaring 9% to $81 per barrel, marking the biggest single-day jump in three years.

Why did BP’s profits decline despite this volatility? The answer lies in BP’s tax burden. The company’s effective tax rate surged from 36% to 50% in Q1 2025 as more profits originated from high-tax jurisdictions. BP’s total tax bill reached $3.1 billion for the period.

BP Business Segments Performance: Gas, Oil Production Face Headwinds

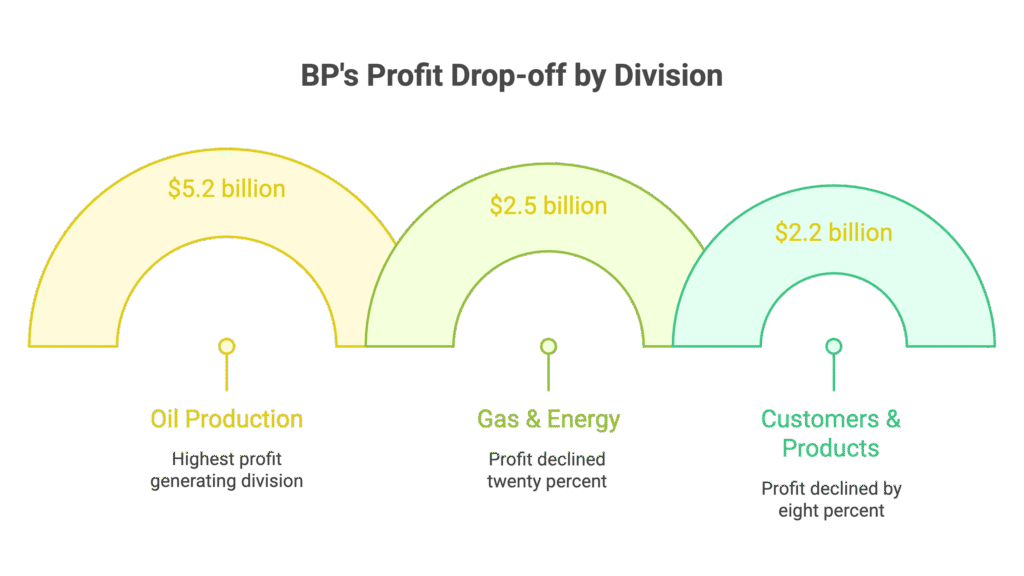

BP’s core business divisions remained profitable in H1 2025, but each segment faced significant challenges:

- BP gas and low carbon energy division: Profit down 20% to $2.5 billion

- BP oil production and operations: Declined 16% to $5.2 billion

- BP customers and products segment: Fell 8% to $2.2 billion

These results reflect broader industry challenges facing oil majors in 2025, yet CEO Murray Auchincloss maintains BP’s “performance improvement” strategy remains on track.

BP Cost-Cutting Strategy: Elliott Management Pushes for $5 Billion More in Savings

Activist investor Elliott Management continues pressuring BP to accelerate cost reductions beyond CEO Murray Auchincloss’s existing target. BP aims to achieve $4-5 billion in structural cost savings by 2027, but Elliott wants another $5 billion on top. BP’s cost-cutting progress in 2025 shows momentum — the company eliminated $938 million in structural costs during H1 2025, building on $750 million saved in 2024.

Auchincloss told the Financial Times that BP will conduct a “thorough review” of operations alongside incoming chairman Albert Manifold. This signals more BP job cuts ahead — the oil major already eliminated 4,700 positions and reduced contractor headcount by 3,000 in 2025.

Here’s where BP’s modernisation gets interesting — the company’s partnering with AI chipmaker Nvidia (valued at $4 trillion) to streamline operations and “reduce cycle time.” This collaboration, announced after Nvidia’s partnership with PM Keir Starmer at London Tech Week 2025, represents BP’s push to leverage artificial intelligence for operational efficiency.

BP Brazil Oil Discovery: Largest Find in 25 Years Boosts Growth Outlook

BP announced its biggest oil discovery in 25 years off Brazil’s Atlantic coast on Monday, marking a pivotal moment for the British oil giant’s growth strategy. This deepwater discovery adds substantial long-term value to BP’s portfolio and reinforces CEO Auchincloss’s renewed focus on traditional hydrocarbon assets.

eToro analyst Lale Akoner notes: “BP is clearly leaning back into its oil roots, which is positive for investors.” BP started five major projects and achieved 10 exploration discoveries in the first six months of 2025, demonstrating strong operational momentum despite the energy transition narrative.

BP Investment Outlook: Balancing Shareholder Returns with Growth

BP’s Q2 2025 results reveal a complex investment case — declining profits offset by strong shareholder returns and promising exploration success. The company’s maintaining its $750 million quarterly buyback programme whilst increasing dividends, demonstrating commitment to investor returns despite operational headwinds.

Hargreaves Lansdown’s Derren Nathan highlights BP’s “financial discipline” as net debt falls and cost savings accelerate. However, with BP production expected to decline in 2025, management remains cautious about expanding capital returns beyond current levels.

For investors evaluating BP shares versus competitors like Shell, the company’s strategy is clear: prioritise traditional oil and gas assets, aggressively cut costs, and maintain steady shareholder distributions whilst navigating volatile energy markets. BP’s Brazilian discovery could prove transformative, but near-term challenges remain.

Looking ahead, BP’s success hinges on executing its cost reduction programme, capitalising on new oil discoveries, and managing the balance between energy transition commitments and traditional hydrocarbon profits.

FAQ

Q1: Why did BP shares rise despite lower profits?

A: Investors cheered BP’s $750 million buyback programme and 4% dividend increase. The company also beat analyst expectations with Q2 profit of $2.4 billion versus the $1.8 billion consensus.

Q2: How is BP using AI technology to improve operations?

A: BP’s partnering with Nvidia to streamline operations and “reduce cycle time.” It’s part of CEO Auchincloss’s push to modernise operations whilst cutting costs.

Q3: What’s BP’s cost-cutting target?

A: BP aims to slash $4-5 billion by 2027, with activist investor Elliott Management pushing for an additional $5 billion. The company’s already cut nearly $1 billion in H1 2025.

Q4: How significant is BP’s Brazilian oil discovery?

A: It’s BP’s largest find in 25 years — a major deepwater discovery that signals the company’s renewed focus on traditional oil operations over aggressive energy transition plans.

Q5: What happened to BP’s tax rate?

A: BP’s effective tax rate jumped from 36% to 50% in Q1 2025 as more profits came from high-tax regions, squeezing overall profitability despite stable revenues.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.