Picture this: you’re 55, ready to tap into your pension for the first time, and HMRC slaps you with an emergency tax bill that assumes you’ll be withdrawing the same massive amount every month for the rest of the year. Spoiler alert: you won’t be.

This HMRC pension emergency tax system has left thousands of pension savers seriously out of pocket. In 2023-24 alone, 6,000 people successfully claimed pension tax refunds after HMRC overcharged them on pension withdrawals—that’s a 20% jump from the year before. We’re talking about some eye-watering emergency tax refund amounts here, with the biggest pension withdrawal refunds hitting six figures.

Here’s why this HMRC pension tax chaos is happening and what you need to know to avoid getting caught in HMRC’s emergency tax trap on pension withdrawals.

HMRC Pension Tax Overcharge Statistics: The Eye-Watering Numbers

The Royal London pension tax refund data paints a stark picture of HMRC overcharging. Around 2,400 savers managed to claw back more than £10,000 each in emergency tax refunds, whilst 11,700 got £5,000+ returned from HMRC pension tax overcharges. The average pension emergency tax refund? £3,342—up £280 from the previous year.

The top 25 emergency tax refunds averaged £106,897. That’s not pocket change—that’s life-changing money sitting in HMRC’s coffers whilst it should be in retirees’ bank accounts.

Clare Moffat from Royal London stated: “Not only do these emergency taxes usually come as a massive shock, the unexpected pension tax amount can also scupper people’s carefully laid plans.”

How HMRC Emergency Tax on Pension Withdrawals Works

Since 2015, pension withdrawal rules let you access some or all of your defined contribution pension savings from age 55. The first 25% comes out tax-free (capped at £268,275), but the remaining 75% gets taxed on pension withdrawals.

Here’s where HMRC pension tax gets problematic. When HMRC doesn’t have a proper tax code for your pension withdrawal, they default to “emergency tax on pensions.” This flawed emergency tax system assumes whatever you withdraw will be your monthly income for the entire tax year.

Why Emergency Tax Creates Pension Overcharges

So if you take out £50,000 as a one-off pension withdrawal, HMRC emergency tax treats you as if you’re earning £50,000 every single month. It’s like assuming someone who buys a car will purchase the same car every week for a year. Makes no sense for pension withdrawals, right?

The HMRC Pension Tax Refund Process: Paperwork Prison

Want your emergency tax refund on pension withdrawals back quickly? Better hope you’ve got your HMRC refund forms sorted. HMRC makes you fill out specific paperwork to get faster pension tax refunds. Miss this step, and you’re stuck waiting until they review everything at the end of the tax year.

That could mean being out of pocket for months—not exactly ideal whilst you’re trying to fund your retirement or handle a financial emergency with your pension withdrawal.

Why HMRC Emergency Tax Problems on Pension Withdrawals Are Getting Worse

HMRC recently announced they’ll overhaul their emergency pension tax system, promising quicker pension tax refunds. Sounds great, except they’re not actually stopping the pension tax overcharging in the first place.

The kicker: HMRC emergency tax issues might get worse. With pensions now subject to inheritance tax, more people are considering withdrawing larger lump sums to avoid passing tax problems to their children. More big pension withdrawals = more emergency tax disasters on pension withdrawals.

“The problem of emergency taxes on pension withdrawals isn’t going away, and there’s a chance it could get worse,” warns Moffat.

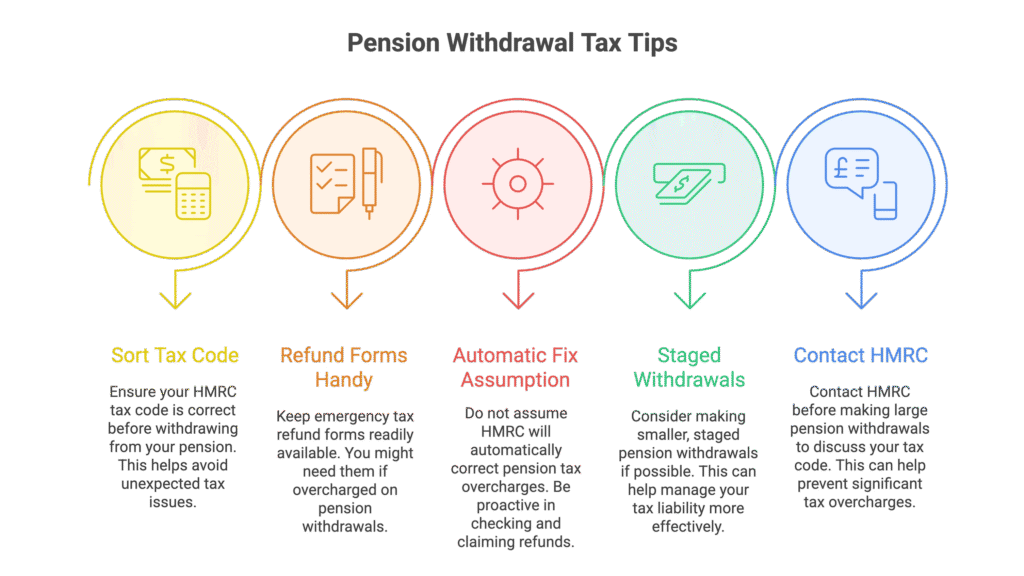

How to Avoid HMRC Emergency Tax on Pension Withdrawals

If you’re planning a pension withdrawal to avoid HMRC emergency tax overcharges:

- Get your HMRC tax code sorted before making pension withdrawals

- Keep those emergency tax refund forms handy

- Don’t assume HMRC will automatically fix pension tax overcharges

- Consider smaller, staged pension withdrawals if possible

- Contact HMRC before large pension withdrawals to discuss tax codes

The bottom line? HMRC’s emergency pension tax system is broken, and until they actually fix the root cause of pension tax overcharges, thousands more savers will keep getting caught in this expensive emergency tax trap.

FAQ: HMRC Pension Emergency Tax and Refunds

Q1: How long does it take to get an emergency tax refund from HMRC on pension withdrawals?

A: It depends on whether you complete the right HMRC pension tax refund forms immediately. With proper paperwork, emergency tax refunds come faster, but without it, you could wait until the end of the tax year—potentially months for your pension tax refund.

Q2: Can I avoid HMRC emergency tax on pension withdrawals entirely?

A: Yes, by ensuring HMRC has the correct tax code for your pension before you withdraw. Contact HMRC in advance to set up proper tax codes for pension withdrawals to avoid emergency tax.

Q3: What’s the biggest HMRC emergency tax refund on pension withdrawals on record?

A: Some individuals have received emergency tax refunds on pension withdrawals exceeding £100,000, with the top 25 pension tax refunds in 2023-24 averaging £106,897 each from HMRC overcharges.

Q4: Will the new inheritance tax rules make HMRC emergency tax on pensions worse?

A: Likely yes. More people may make larger lump sum pension withdrawals to avoid passing tax burdens to their heirs, triggering more HMRC emergency tax situations on pension withdrawals.

Q5: Is the 25% tax-free pension allowance affected by HMRC emergency tax?

A: No, the first 25% of your pension withdrawal (up to £268,275) remains tax-free. HMRC emergency tax only applies to the taxable portion of your pension withdrawal above this threshold.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.