Banking Tax Revolt: Why UK’s Biggest Banks Are Fighting Back

Here’s a number that’ll make you wince: UK banks already face a whopping 45.8% tax rate—nearly double what their New York rivals pay. Now, with Chancellor Rachel Reeves eyeing a £20bn budget black hole, Britain’s banking titans are practically staging an intervention.

The message from Barclays, Citi, and JP Morgan? Touch that bank tax dial again, and you might just kill the golden goose that keeps London’s financial services competitive with Wall Street.

Barclays Boss Pulls No Punches on Tax Policy

CS Venkatakrishnan (everyone calls him Venkat) didn’t mince words when he told CNBC: “Milking the financial sector is not good, because it stifles investment.”

His point? London sits alongside New York as one of the world’s two financial powerhouses. Why would you want to “tax it out of existence”?

Venkat’s been beating this drum for months, pointing out that UK banks already pay significantly more than their overseas competitors. It’s like asking Usain Bolt to run with ankle weights—sure, he might still win, but why handicap your best performer?

Citi and JP Morgan Join the Chorus

Tiina Lee from Citi Bank echoed the concerns, noting that markets are getting “impatient” for clarity on tax policy. Her clients want one thing: a stable, competitive tax regime that doesn’t change every budget cycle.

Meanwhile, JP Morgan’s Conor Hillery struck a more optimistic tone, calling recent US investment in London a “vote of confidence in the UK.” He’s right—London remains Europe’s premier capital market, even with its current tax burden.

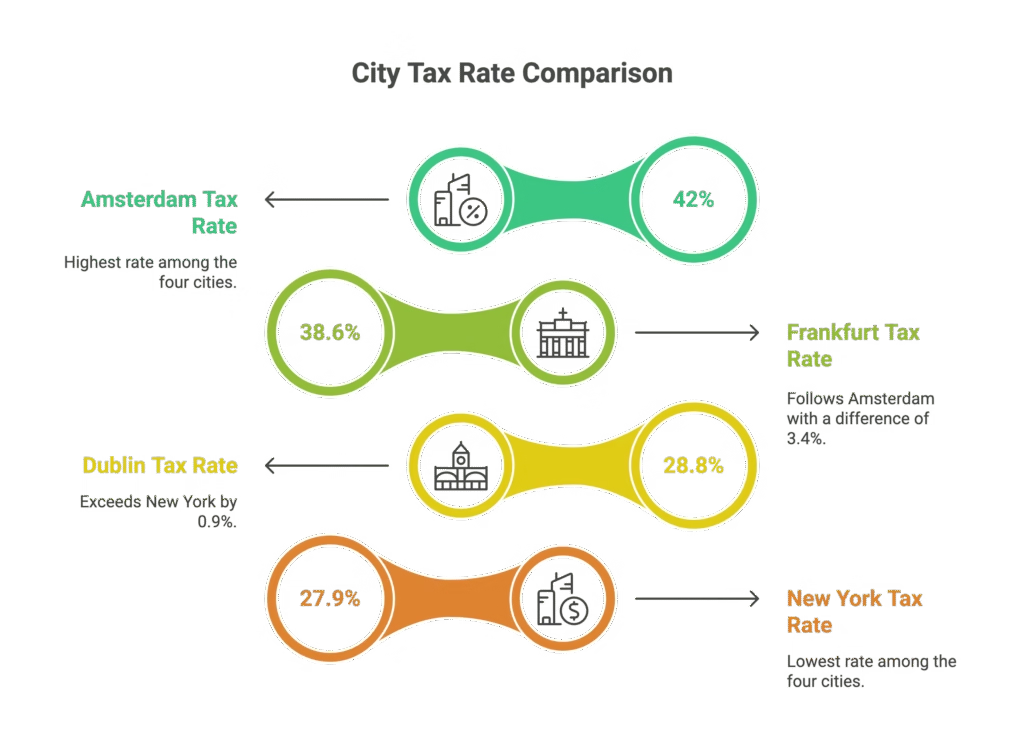

The Numbers Game: How UK Banks Stack Up

Let’s talk cold, hard facts. UK banks face a 45.8% total tax rate compared to:

- Amsterdam: 42%

- Frankfurt: 38.6%

- Dublin: 28.8%

- New York: 27.9%

That’s not exactly what you’d call a level playing field.

The Political Reality Check

Here’s the bind Reeves finds herself in: she needs cash (£20bn worth), and banks look like easy targets. Think tanks and politicians keep floating bank taxes as “politically safe” revenue grabs.

But there’s a catch. The Treasury wants financial services at the “heart” of economic growth. Hard to do that while simultaneously squeezing the life out of them with higher taxes.

It’s like telling someone you want them to be your business partner while picking their pockets—mixed messages, much?

What This Means for London’s Financial Future

The banking chiefs aren’t just protecting their bottom lines here. London’s financial sector employs hundreds of thousands and generates massive tax revenue even at current rates.

Push too hard, and those jobs and investment dollars might start looking at Dublin or Frankfurt—where the tax grass is notably greener.

Key Takeaways

Banking executives from Britain’s biggest lenders have drawn a clear line in the sand over potential tax hikes. With UK banks already paying 45.8% compared to just 27.9% in New York, further increases could push investment and jobs overseas. Rachel Reeves faces a tough choice: quick revenue or long-term financial sector growth.

Ready to stay ahead of banking regulation and UK financial policy? Subscribe to our weekly newsletter.

FAQ

Q1: Why are UK banks taxed so heavily compared to other countries?

A: UK banks face a combination of corporation tax, banking surcharge, and other levies that push their total rate to 45.8%. This reflects both revenue needs and political sentiment following the 2008 financial crisis.

Q2: Could banks actually leave London if taxes increase further?

A: While complete relocation is unlikely, banks could shift operations, jobs, and investment to lower-tax jurisdictions like Dublin or Frankfurt. Even partial moves would hurt London’s economy.

Q3: How much revenue would a new bank tax actually raise?

A: Estimates vary, but economists suggest it could generate several billion pounds annually. However, this assumes banks don’t reduce operations or find ways to minimise their UK tax exposure.

Q4: What’s Rachel Reeves’ biggest challenge with bank taxation?

A: Balancing immediate revenue needs against long-term competitiveness. Higher taxes might solve short-term budget problems but could undermine London’s position as a global financial centre.

Q5: Are there alternatives to raising bank taxes?

A: Yes, the government could explore other revenue sources, spending cuts, or structural reforms to banking regulation that generate revenue without hurting competitiveness.

DISCLAIMER

Effective Date: 15th July 2025

The information provided on this website is for informational and educational purposes only and reflects the personal opinions of the author(s). It is not intended as financial, investment, tax, or legal advice.

We are not certified financial advisers. None of the content on this website constitutes a recommendation to buy, sell, or hold any financial product, asset, or service. You should not rely on any information provided here to make financial decisions.

We strongly recommend that you:

- Conduct your own research and due diligence

- Consult with a qualified financial adviser or professional before making any investment or financial decisions

While we strive to ensure that all information is accurate and up to date, we make no guarantees about the completeness, reliability, or suitability of any content on this site.

By using this website, you acknowledge and agree that we are not responsible for any financial loss, damage, or decisions made based on the content presented.